💳 Credit & Debt Management Hub

Credit and debt management are essential parts of building long-term financial stability. Your ability to understand how credit works, manage borrowing responsibly, and repay debt strategically affects everything from qualifying for a mortgage to securing lower interest rates and reducing financial stress.

This section of Jason’s Fin Tips provides practical, educational guidance designed to help you understand credit, manage debt effectively, and strengthen your financial foundation.

Here you will learn how to:

• Understand your credit score and the factors that influence it

• Manage debt strategically while avoiding common borrowing pitfalls

• Explore debt consolidation options that align with your financial goals

• Rebuild damaged credit and restore your financial reputation

• Borrow responsibly to support long-term financial stability

🔍 Why Credit & Debt Management Matters

Poor credit habits can lead to higher borrowing costs, loan denials, and long-term financial setbacks. For example, a lower credit score can increase the cost of a mortgage by thousands of dollars over the life of a loan. High credit card balances can also raise your credit utilization ratio, which may reduce your credit score and make borrowing more expensive.

With the right knowledge and habits, however, credit can become a powerful financial tool rather than a source of stress.

At Jason’s Fin Tips, we equip you with:

✅ Step-by-step strategies to boost your credit score

✅ Proven methods for paying off credit card debt

✅ Insights into debt consolidation tools and techniques

✅ Tips to repair and rebuild damaged credit

✅ Guidance on borrowing smart and staying debt-free

🎯 Your Path to Financial Freedom Starts Here

Mastering credit and debt management isn’t just about numbers—it’s about regaining confidence and building a future free from financial anxiety.

These skills are the foundation for:

• Reaching major life goals like buying a home, starting a business, or retiring comfortably

• Reducing debt-related stress

• Building wealth over time

The guides below explore the most important areas of credit and debt management, from understanding how credit scores work to developing effective repayment strategies and rebuilding financial stability.

🧭 Your Credit & Debt Management Roadmap (Start Here)

If you’re not sure where to begin, follow this step-by-step roadmap. Each phase builds on the previous one—helping you move from financial stress to long-term stability and wealth.

Each step below links to a deeper guide so you can take action immediately.

🔥 Credit Roadmap at a Glance

| Phase | Focus | Key Action | Outcome |

|---|---|---|---|

| 1. Awareness | Understand your credit | Check reports & score | Clarity |

| 2. Control | Stop financial damage | Pay on time, lower utilization | Stability |

| 3. Optimization | Reduce high-interest debt | Pay off strategically | Savings |

| 4. Growth | Build stronger credit | Use tools + consistency | Higher score |

| 5. Leverage | Use credit wisely | Borrow strategically | Better terms |

| 6. Expansion | Build wealth | Save & invest | Financial freedom |

🔹 Phase 1: Understand Where You Stand (Awareness)

Goal: Build clarity before taking action

Key Actions:

- Check your credit score (FICO, VantageScore)

- Review your credit reports

- Identify errors, negative marks, and high balances

Why It Matters:

You can’t improve what you don’t measure.

👉 Start Here:

- How to Check Your Credit Score (Step-by-Step Guide)

- How to Read Your Credit Report and Fix Errors

🔹 Phase 2: Stabilize Your Financial Foundation (Control)

Goal: Stop further damage and regain control

Key Actions:

- Make all payments on time

- Reduce credit utilization below 30% (ideally under 10%)

- Avoid unnecessary new accounts

- Build a small emergency fund ($500–$1,000)

Why It Matters:

This phase protects your financial foundation and prevents setbacks.

👉 Start Here:

- How to Lower Your Credit Utilization Quickly

- How to Build a Starter Emergency Fund (Fast)

🔹 Phase 3: Attack High-Interest Debt (Optimization)

Goal: Reduce the cost of debt and accelerate progress

Strategies:

- Debt Avalanche (highest interest first)

- Debt Snowball (smallest balance first)

- Balance transfers

- Negotiating interest rates

Why It Matters:

High-interest debt is one of the biggest obstacles to financial progress.

👉 Start Here:

- Strategies to Pay Off Credit Card Debt Faster

- How to Negotiate Lower Interest Rates on Loans

🔹 Phase 4: Rebuild and Strengthen Credit (Growth)

Goal: Improve your credit profile over time

Key Actions:

- Use secured credit cards or credit-builder loans

- Keep balances low

- Maintain long account history

- Diversify credit types responsibly

Why It Matters:

A stronger credit profile lowers borrowing costs and expands opportunities.

👉 Start Here:

- How to Rebuild Credit After Financial Setbacks

- Best Credit-Building Tools for Beginners

🔹 Phase 5: Optimize Borrowing Strategy (Leverage)

Goal: Use credit intentionally as a financial tool

Key Actions:

- Borrow with a clear purpose

- Compare rates and loan terms carefully

- Understand your debt-to-income (DTI) ratio

- Align borrowing with long-term goals

Why It Matters:

Smart borrowing supports your financial plan—poor borrowing undermines it.

👉 Start Here:

- How to Choose the Right Loan (Without Overpaying)

- Understanding Debt-to-Income Ratio and Why It Matters

🔹 Phase 6: Transition to Wealth Building (Expansion)

Goal: Move beyond debt into long-term financial growth

Key Actions:

- Redirect debt payments into savings and investing

- Build retirement accounts (IRA, 401(k))

- Increase financial flexibility and resilience

Why It Matters:

Debt management is not the finish line—wealth building is.

👉 Start Here:

Beginner’s Guide to Building Long-Term Wealth

Debt management is not the finish line—wealth building is.

How to Start Investing After Paying Off Debt

Key Topics in Credit & Debt Management

📊 Understanding Credit Scores and Reports

Your credit score is more than just a number—it’s a key to financial opportunity. From qualifying for a mortgage to getting the best interest rates on credit cards and auto loans, your score plays a critical role in your financial life.

This section will help you:

- ✅ Understand how credit scores are calculated (FICO, VantageScore, and more)

- ✅ Learn what’s in your credit report—and what lenders look for

- ✅ Improve your credit score with practical, proven steps

- ✅ Identify and dispute errors that may be dragging your score down

- ✅ Monitor your credit to detect fraud and protect your identity

Why It Matters

A strong credit score saves you money and opens doors. By taking control of your credit today, you can build a stronger financial future tomorrow.

Explore our guides to learn how your credit works—and how to make it work for you.

💳 Managing Credit Card Debt Effectively

Credit card debt can accumulate fast—and cost you thousands in interest over time. But with the right strategy, you can take control, pay it down efficiently, and stay ahead of financial stress.

This section will guide you through:

- ✅ 6 Proven Strategies to Conquer Debt and Build Wealth

- ✅ How to reduce interest charges with balance transfers or renegotiated rates

- ✅ Ways to avoid the minimum payment trap and make real progress

- ✅ Smart habits to prevent future credit card debt

- ✅ Tools and apps that make debt tracking easier and more motivating

Why It Matters

Managing credit card debt wisely isn’t just about paying off balances—it’s about regaining financial freedom. By implementing focused strategies, you can reduce your financial burden and redirect money toward savings, investments, or other life goals.

Explore our expert tips and take your first step toward becoming debt-free.

🔄 Debt Consolidation: Options and Considerations

Debt consolidation can be a powerful tool to streamline your finances, reduce interest costs, and regain control of your budget. By combining multiple debts into a single payment, you may simplify your monthly obligations and accelerate your path to becoming debt-free.

In this section, you’ll explore:

- ✅ How debt consolidation works and when it makes sense

- ✅ Options like personal loans, balance transfer credit cards, and home equity solutions

- ✅ The pros and cons of each method—fees, interest savings, and credit score impacts

- ✅ How to choose the right consolidation strategy based on your credit profile and financial goals

- ✅ Warning signs to avoid predatory lenders and high-risk consolidation traps

Why It Matters

When used wisely, debt consolidation can provide breathing room and peace of mind—freeing up cash flow and making your debt more manageable. But the key is choosing a strategy that supports long-term financial stability, not just short-term relief.

Start here to explore your options and build a repayment plan that works for you—not against you.

⚖️ Responsible Borrowing & Avoiding Excessive Debt

Borrowing can be a smart financial tool—when used intentionally and within your means. But without clear boundaries, it can quickly spiral into high-interest debt and financial instability.

This section will help you:

- ✅ Understand your debt capacity and how much borrowing is sustainable

- ✅ Evaluate loans based on terms, rates, and long-term impact

- ✅ Identify and avoid predatory lenders and deceptive loan offers

- ✅ Learn the difference between “good debt” vs. “bad debt”

- ✅ Make informed decisions that support your overall financial plan

Why It Matters

Responsible borrowing isn’t about avoiding all debt—it’s about borrowing with purpose. Whether it’s a student loan, auto loan, or mortgage, taking on debt should align with your goals and ability to repay. This mindset protects your credit, preserves your options, and ensures long-term financial resilience.

🛠️ Credit Repair Techniques & Rebuilding Credit

Rebuilding your credit takes time—but the right techniques can accelerate your progress and restore financial confidence. Whether you’re recovering from past challenges or fixing reporting errors, effective credit repair begins with a plan.

In this section, you’ll learn how to:

- ✅ Identify and dispute inaccurate items on your credit report

- ✅ Negotiate with creditors to settle or remove negative marks

- ✅ Use secured credit cards or credit-builder loans to reestablish a positive history

- ✅ Prioritize on-time payments and low utilization ratios to steadily raise your score

- ✅ Monitor your credit and avoid pitfalls that can undo your progress

Why It Matters

A strong credit score opens doors—to lower interest rates, better loan terms, and increased financial flexibility. By taking control of your credit repair process, you’re not just fixing numbers—you’re rebuilding your financial future.

6 Strategies to Conquer Debt and Build Wealth

Learn six practical budgeting methods designed to help households regain control of spending, reduce debt, and build long-term financial stability.

→ Explore the Conquer Debt Budgeting Guide

Latest Credit & Debt Management Articles

Explore the latest educational articles from the Credit & Debt Management blog. These guides provide deeper insights into credit scores, borrowing strategies, debt repayment methods, and financial decision-making.

-

How to Negotiate Better Loan Rates — Insider Strategies to Lower Your Borrowing Costs

💡 Quick Answer: How Do You Actually Negotiate a Loan Rate? Yes—you can negotiate loan rates, especially with banks and lenders who want your business.The key is to bring competing offers, show strong financials, and ask directly using clear, confident language. ✅ Most Effective Approach 👉 Even a 0.25% reduction can save thousands over time, […]

-

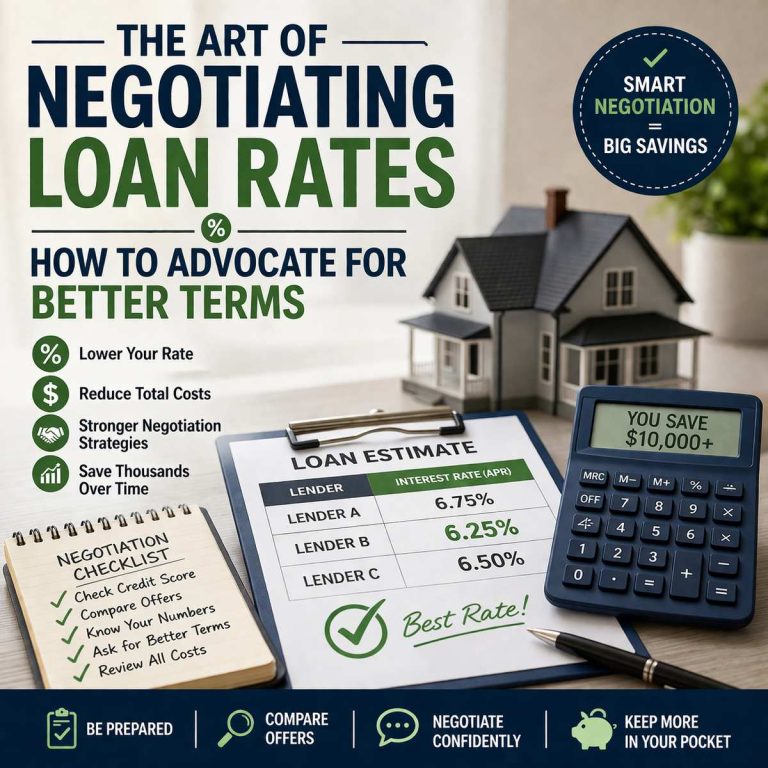

The Art of Negotiating Loan Rates – How to Advocate for Better Terms

1. 💡 Quick Answer: Best Tips for Negotiating Loan Rates 👉 Even small improvements—like a 0.5% rate reduction—can save thousands over the life of a loan. 2. 🧭 Introduction — Mastering the Art of Loan Negotiation In a high-rate environment like 2025, negotiation isn’t just smart — it’s essential. Even modest rate reductions can translate […]

-

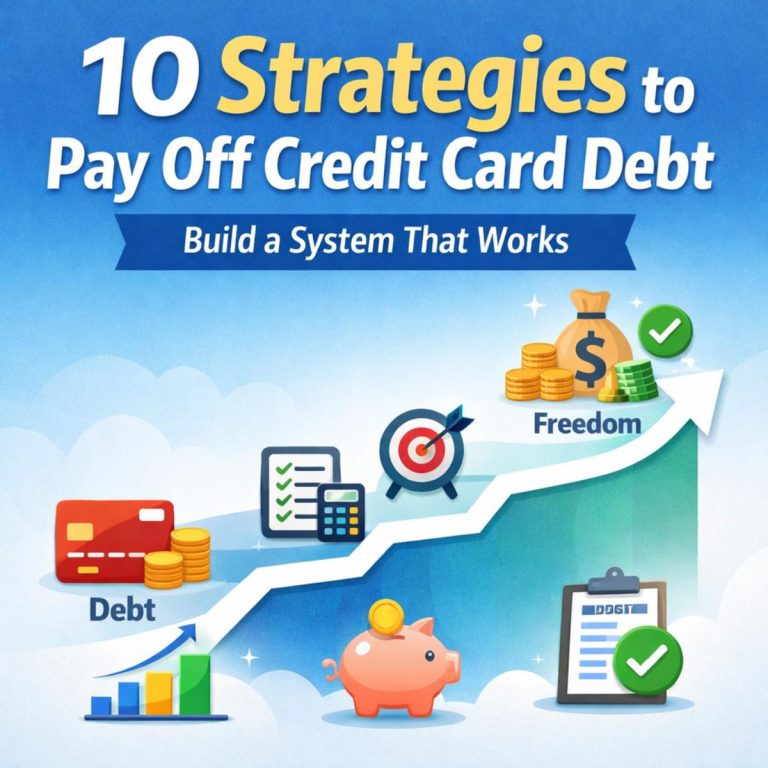

10 Proven Credit Card Payment Strategies to Pay Off Debt Faster (And Build a System That Works)

⚡ Quick Answer: How to Pay Off Credit Card Debt The fastest way to pay off credit card debt is to follow a clear, consistent system: 👉 The key to success isn’t choosing the “perfect” strategy—it’s choosing one you can follow consistently over time. 🔥 Key Takeaways 🧭 How to Tackle Credit Card Debt Step-by-Step […]

-

How Credit Utilization Impacts Your Score and Ways to Improve It

Introduction What is Credit Utilization?Credit utilization is a critical factor that directly influences your credit score. It refers to the percentage of your available credit limit that you’re using at any given time. For example, if you have a credit card with a $10,000 limit and a $2,000 balance, your utilization is 20%. Understanding and […]

-

Credit Utilization Explained: How to Lower It Fast and Improve Your Score

🧭 Introduction – Why Credit Utilization Matters More Than You Think Credit utilization is one of the most powerful—yet often overlooked—factors influencing your credit score. At its core, it represents how much of your available revolving credit you are currently using. While it may seem like a simple percentage, it plays a critical role in […]

-

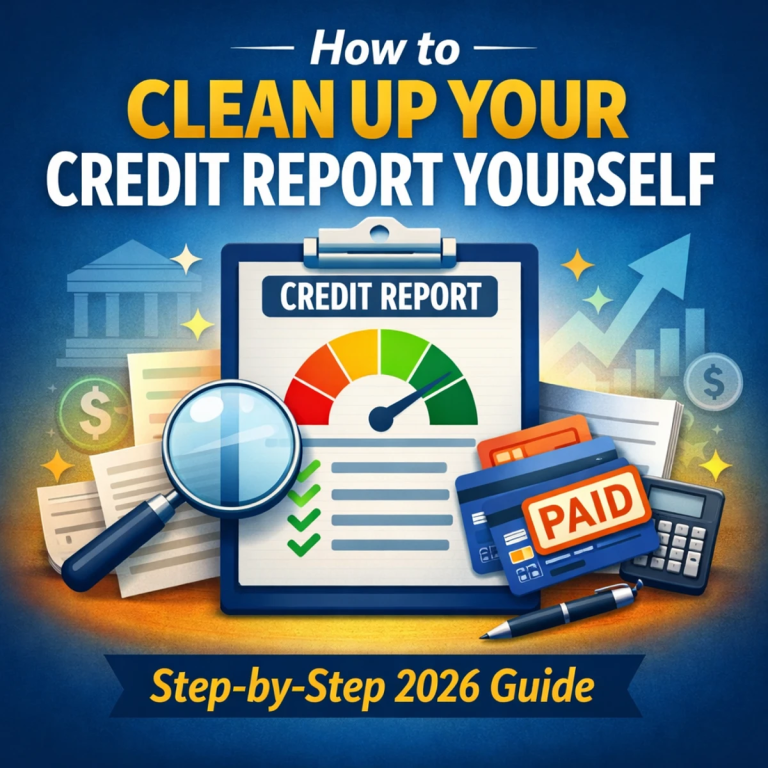

How to Clean Up Your Credit Report Yourself (Step-by-Step 2026 Guide)

I. Introduction — Take Control of Your Credit Without Paying Anyone Else If you’ve ever looked at your credit score and wondered, “How do I clean this up?”, you’re not alone. Millions of people assume that fixing credit requires expensive services, secret tricks, or years of waiting. In reality, most credit repair is simply about […]

🔗 Explore Related Financial Topics

Credit decisions influence many areas of personal finance, from borrowing and homeownership to long-term saving and investing. Continue exploring these related financial topics to strengthen your financial foundation.

- Budgeting & Money Management – Understand how spending habits and budgeting systems affect credit usage and debt repayment strategies.

- Student Loans – Learn how education debt impacts credit, repayment planning, and long-term financial stability.

- Mortgages & Homeownership – Explore how credit scores, debt ratios, and borrowing history influence mortgage eligibility and home financing.

- Saving & Investing – Once debt is under control, saving and investing help build long-term financial security and wealth.

- Financial Education & Literacy – Strengthen your understanding of credit systems, interest, and financial decision-making.

About the Author — Jason Bryan Ball

Financial Educator | Founder of Jason’s Fin Tips

Read more about Jason Bryan Ball →