💳 Managing Credit Card Debt Effectively

Take Control of High-Interest Debt and Build Financial Stability

Credit card debt is one of the most common—and costly—forms of consumer debt. With average APRs often exceeding 20%, even small balances can grow quickly if left unmanaged.

This section is designed to help you:

- Reduce high-interest balances efficiently

- Choose the right repayment strategy

- Avoid costly mistakes that keep you in debt

- Build habits that support long-term financial stability

👤 Who This Page Is For

This section is designed for individuals who want a clear, structured approach to managing and eliminating credit card debt.

You’ll benefit most from this guide if you:

- Carry a credit card balance month-to-month

- Feel stuck making minimum payments without real progress

- Have multiple credit cards with different interest rates

- Want a step-by-step system to regain control of your finances

- Are looking to improve your credit score while reducing debt

- Prefer practical, actionable strategies over generic advice

👉 Whether you’re just starting your debt payoff journey or refining your strategy, this page provides a framework you can follow with confidence.

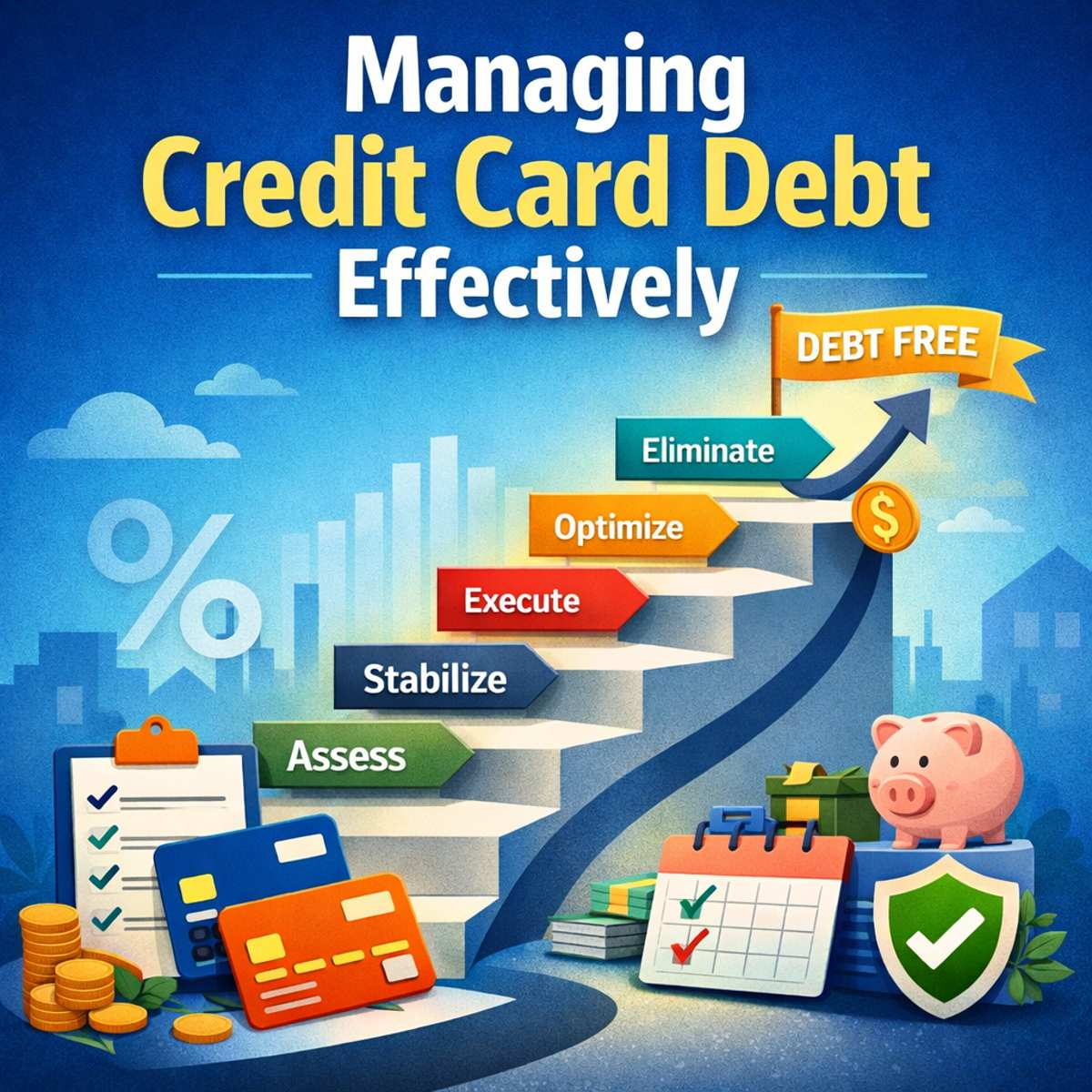

🧭 Start Here: Credit Card Debt Payoff Roadmap

If you’re unsure where to begin, follow this structured approach. Each phase builds on the previous one—helping you move from financial stress to long-term control.

📊 Credit Card Debt Payoff Roadmap

| Step | Focus | What To Do | Outcome |

|---|---|---|---|

| 1. Assess | Understand your full debt picture | List all balances, APRs, minimum payments, and due dates | Clarity |

| 2. Stabilize | Stop the debt from growing | Pause new charges, create a basic spending plan, identify leaks | Stability |

| 3. Strategize | Choose your payoff method | Select a strategy (Snowball, Avalanche, or your custom system) | Direction |

| 4. Execute | Build consistent momentum | Pay more than the minimum, automate payments, track progress | Progress |

| 5. Optimize | Reduce costs and accelerate payoff | Lower interest rates, use balance transfers carefully, increase payments | Savings |

| 6. Eliminate | Become debt-free and stay there | Pay off remaining balances and build safeguards to avoid relapse | Financial Freedom |

🔍 How to Use This Roadmap

- Start where you are — Don’t skip ahead if your foundation isn’t stable

- Focus on one phase at a time — Trying to do everything at once leads to burnout

- Revisit each step monthly — Your situation will evolve as balances decrease

👉 This is not a one-time checklist—it’s a repeatable system you refine over time.

🔗 Deep Dive Into Each Step

- 👉 Assess Your Debt: How to List and Organize Your Credit Card Balances

- 👉 Stabilize Your Finances: How to Stop Overspending and Control Cash Flow

- 👉 Choose a Strategy: 10 Strategies to Pay Off Credit Card Debt Faster

- 👉 Execute Your Plan: How to Stay Consistent and Avoid Setbacks

- 👉 Optimize Your Debt: Balance Transfers, Rate Negotiation, and Interest Reduction

- 👉 Eliminate and Maintain: How to Stay Debt-Free Long-Term

💡 Pro Insight: Why This Works

Most people fail at debt repayment not because they lack effort—but because they lack structure.

This roadmap:

- Aligns behavior with long-term financial goals

- Removes decision fatigue

- Creates a clear starting point

- Builds momentum through small wins

🎯 What You’ll Learn in This Section

Here we focuses specifically on managing revolving credit and eliminating high-interest debt:

- How credit card interest and APR actually work

- Why minimum payments keep you in long-term debt

- Proven strategies to accelerate payoff

- How to use balance transfers strategically

- How credit utilization impacts your credit score

- Behavioral habits that prevent debt cycles

🚀 Featured Guide: Start With This

👉 10 Strategies to Pay Off Credit Card Debt (and Stay Debt-Free)

If you only read one guide in this section, start here. This comprehensive post walks you through:

- Step-by-step payoff strategies

- Real-world examples

- Actionable systems you can implement immediately

Understanding Credit Card Debt (Core Concepts)

Interest Rates and APR

Learn how interest is calculated, how compounding works, and how even small differences in APR can significantly impact total repayment costs.

Minimum Payments and Compounding Debt

Paying only the minimum may feel manageable—but it dramatically increases repayment time and total interest paid.

⚙️ Debt Payoff Strategies (Your System Matters Most)

Choosing the right strategy is the difference between frustration and progress.

- Expenditure Tracker™ – Build awareness and identify savings opportunities

- Balanced Path™ – Combine quick wins with interest reduction

- EQ Planner™ – Prioritize emotionally stressful debts first

- Summit Strategy™ – Focus on highest interest rates to minimize cost

- Plains Strategy™ – Simplify by eliminating low-interest balances first

- Domino Strategy™ – Build momentum through small wins

👉 The best strategy is the one you can consistently follow.

🔄 Advanced Tactics to Reduce Debt Faster

Balance Transfers and 0% APR Offers

Used correctly, these can significantly reduce interest—but fees and timelines must be carefully managed.

Negotiating Lower Interest Rates

Many lenders are willing to reduce your APR if you ask—especially with a strong payment history.

📊 Credit Score Impact and Optimization

Credit Utilization

Your utilization ratio is one of the most important factors in your credit score.

👉 Aim to keep utilization below 30%—and ideally under 10% for optimal scoring.

⚠️ Avoid These Common Credit Card Traps

- Deferred interest promotions

- Late payment penalties

- High utilization cycles

- Over-reliance on revolving credit

- Predatory lending structures

🧱 Build Better Credit Habits

Long-term success comes from behavior, not just strategy:

- Set realistic spending limits

- Automate payments

- Monitor statements regularly

- Track progress monthly

- Align debt repayment with income

📈 Debt-to-Income (DTI) Awareness

Your debt-to-income ratio plays a key role in:

- Loan approvals

- Interest rates

- Financial flexibility

Managing credit card debt improves both your cash flow and borrowing power.

🧩 Managing Multiple Credit Cards

If you have multiple cards:

- Prioritize high-interest balances

- Keep older accounts open for credit history

- Organize payments to avoid missed due dates

- Avoid spreading balances inefficiently

📰 Explore More in This Section

Check our our most recent blog posts.

-

How to Negotiate Better Loan Rates — Insider Strategies to Lower Your Borrowing Costs

💡 Quick Answer: How Do You Actually Negotiate a Loan Rate? Yes—you can negotiate loan rates, especially with banks and lenders who want your business.The key is to bring competing offers, show strong financials, and ask directly using clear, confident language. ✅ Most Effective Approach 👉 Even a 0.25% reduction can save thousands over time, […]

-

10 Proven Credit Card Payment Strategies to Pay Off Debt Faster (And Build a System That Works)

⚡ Quick Answer: How to Pay Off Credit Card Debt The fastest way to pay off credit card debt is to follow a clear, consistent system: 👉 The key to success isn’t choosing the “perfect” strategy—it’s choosing one you can follow consistently over time. 🔥 Key Takeaways 🧭 How to Tackle Credit Card Debt Step-by-Step […]

-

Credit Utilization Explained: How to Lower It Fast and Improve Your Score

🧭 Introduction – Why Credit Utilization Matters More Than You Think Credit utilization is one of the most powerful—yet often overlooked—factors influencing your credit score. At its core, it represents how much of your available revolving credit you are currently using. While it may seem like a simple percentage, it plays a critical role in […]

-

Strategies to Pay Off Credit Card Debt Faster – Proven Methods to Save Money and Build Momentum

Strategies to Pay Off Credit Card Debt Faster 💳 Credit card debt can feel like a treadmill you can’t step off — the harder you try, the faster the interest seems to pile up.But here’s the truth: with the right plan and consistent habits, you can break the cycle, rebuild confidence, and start using your […]

-

Managing Debt Effectively – Understand the Psychology of Debt and Prioritize Your Payoff Plan

📉 Managing Debt Effectively Debt can be more than a financial burden—it can affect your health, your relationships, and your confidence. But you are not alone, and you are not powerless. This guide will help you understand the emotional roots of debt, how to pick a payoff strategy that works for your mindset, and how […]

-

Understanding the Impact of Minimum Payments on Long-Term Debt

Key Takeaways Introduction Imagine carrying a $5,000 balance on a credit card with a 20% APR. If you make only the minimum payment each month, it could take over a decade to repay the debt, costing you thousands in interest. This example highlights the financial strain of relying on minimum payments—a common but costly mistake. […]

💡 Credit Card Debt Strategy: What Actually Works

Managing credit card debt isn’t just about paying balances—it’s about using the right system and behavior together.

Here’s what actually makes the biggest difference:

1. Interest Matters More Than Balance

High-interest debt grows quickly. Prioritizing higher APR balances can significantly reduce the total cost of repayment over time.

2. Consistency Beats Perfection

You don’t need a perfect plan—you need a consistent one. Regular, above-minimum payments create momentum and reduce long-term interest.

3. Behavior Drives Results

Spending habits matter just as much as repayment strategy. Without controlling new debt, even the best payoff plan can fail.

4. Small Wins Build Momentum

Paying off smaller balances can create psychological motivation, helping you stay committed to the process.

5. Strategy Should Match Your Personality

Some people succeed with mathematically optimal strategies (like high-interest prioritization), while others benefit more from emotionally rewarding approaches.

👉 The most effective strategy is the one you can stick with long enough to succeed.

❓ Frequently Asked Questions (FAQ)

What is the fastest way to pay off credit card debt?

The fastest way typically combines paying more than the minimum with prioritizing high-interest balances (often called the avalanche method). Increasing income or reducing expenses can accelerate the process even further.

Is it better to pay off one card at a time or multiple cards?

Focusing on one card at a time is usually more effective. This allows you to concentrate your payments, build momentum, and reduce complexity while still making minimum payments on other accounts.

How much should I pay beyond the minimum payment?

Even small increases—such as paying 10% to 20% more than the minimum—can significantly reduce the total interest paid and shorten your repayment timeline.

Do balance transfers help reduce credit card debt?

Balance transfers can be helpful if used strategically, especially with 0% introductory APR offers. However, fees, time limits, and the risk of accumulating new debt must be carefully managed.

How does credit card debt affect my credit score?

Credit card debt primarily impacts your credit score through your credit utilization ratio. High balances relative to your credit limit can lower your score, while reducing balances can improve it.

Should I close credit cards after paying them off?

In most cases, it’s better to keep older accounts open. Closing cards can reduce your available credit and negatively impact your credit utilization and credit history length.

What’s the biggest mistake people make with credit card debt?

One of the most common mistakes is continuing to use credit cards while trying to pay them off. This creates a cycle that prevents meaningful progress.