💡 Simple Family Budget Plan (Quick Start Today)

If you want a practical way to take control of your family finances, start with this simple, repeatable budgeting process:

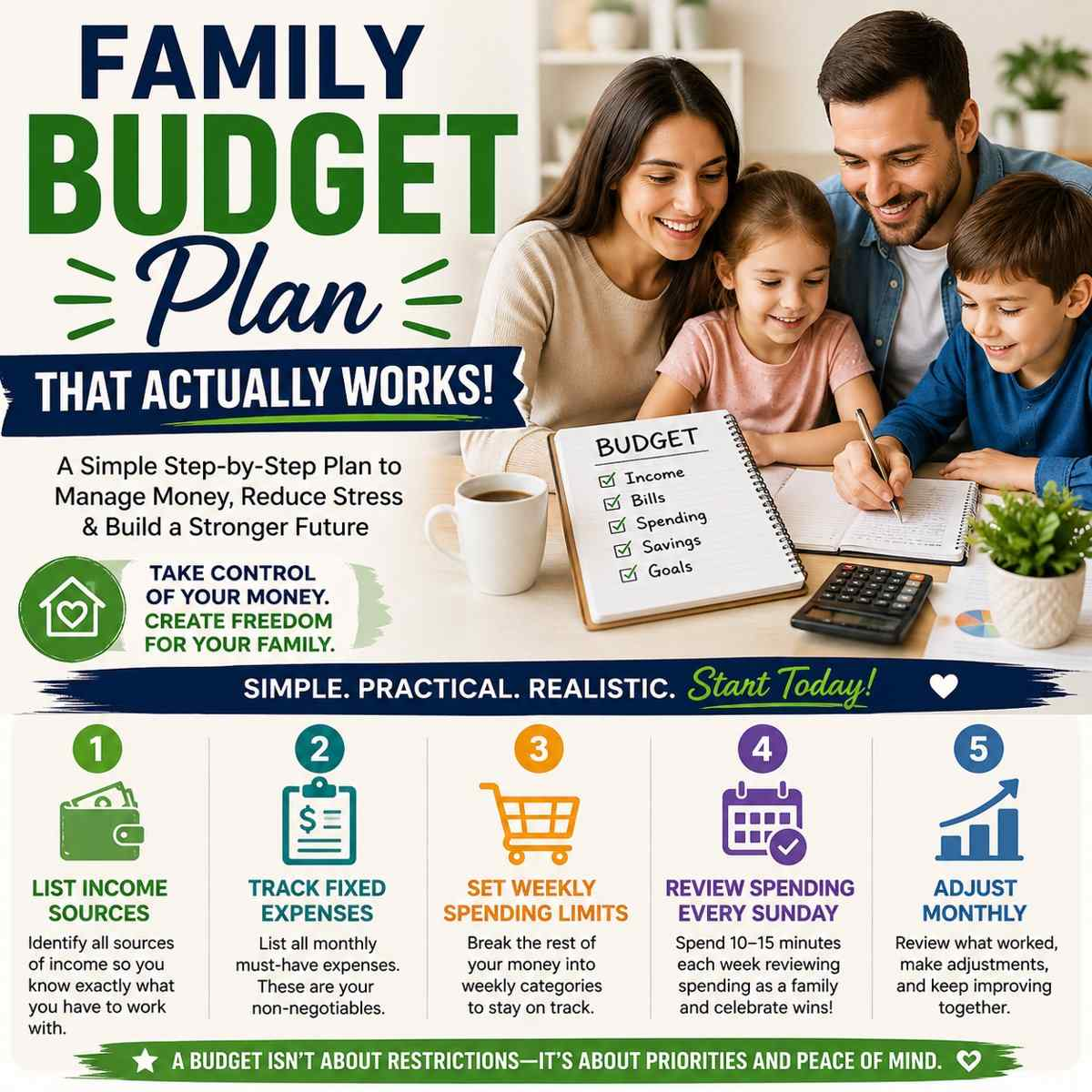

1. List All Income Sources

Identify every source of household income, including salaries, side income, benefits, and irregular earnings.

👉 This gives you a clear starting point for what you can realistically spend and save.

2. Track Fixed Expenses

Write down all consistent monthly costs such as rent or mortgage, utilities, insurance, childcare, and subscriptions.

👉 These are your non-negotiables and form the foundation of your budget.

3. Set Weekly Spending Limits

Break your remaining income into weekly spending categories like groceries, gas, and discretionary spending.

👉 Weekly limits are easier to manage and help prevent overspending early in the month.

4. Review Spending Every Sunday

Set aside 10–15 minutes each week to review your spending as a family.

👉 This builds awareness, accountability, and keeps everyone aligned.

5. Adjust Monthly

At the end of each month, evaluate what worked and what didn’t—then refine your budget.

👉 Budgeting is a living process, not a one-time task.

🎯 Why This Works

- Simple and actionable — easy for families to start immediately

- Flexible — adapts to changing income and expenses

- Proactive — helps catch overspending before it becomes a problem

- Collaborative — encourages family involvement and accountability

🚀 Pro Tip

Start small. Even following this process for one month can reveal spending patterns and opportunities to save that you may not have noticed before.

💡 1. Family Finance – Creating a Budget That Works for the Whole Family

It’s the end of the month, and the Smith family sits around the kitchen table, surrounded by receipts and unpaid bills. The parents are anxious, wondering where their paycheck disappeared to, while the kids remain blissfully unaware of the financial strain. Sound familiar? You’re not alone—millions of families face this same moment of financial confusion every month.

But it doesn’t have to be this way.

A thoughtful family budget can turn financial chaos into confidence. Instead of stress and uncertainty, you gain a clear plan for how your money is earned, spent, and saved—together as a family.

Budgeting isn’t just about numbers or spreadsheets—it’s about communication, priorities, and shared goals. It helps families:

- Build stability through predictable spending.

- Prepare for emergencies and long-term needs.

- Teach children lifelong money skills.

- Strengthen trust and teamwork in financial decisions.

In this guide, we’ll walk you through every step of creating a realistic, flexible budget that works for your entire household. Whether you’re managing dual incomes, raising young children, or planning for college tuition, you’ll learn how to design a system that empowers everyone—from parents to kids—to make smarter financial choices and build lasting security together.

A well-crafted family budget can transform this all-too-familiar chaos into clarity and financial security, offering peace of mind and a stable foundation for the future.

💡 2. Key Takeaways

1. Budgeting as a Family Affair

Engaging every family member in the budgeting process builds awareness, teamwork, and accountability. When everyone understands the plan, financial goals become shared achievements rather than individual burdens.

2. Setting Realistic Financial Goals

Balance short-term wins—like saving for a trip or paying off small debts—with long-term goals such as retirement or college funding. Realistic milestones keep your family motivated and financially resilient.

3. Choosing the Right Budgeting Method

There’s no universal formula. Test approaches like the Envelope System, Zero-Based Budgeting, or the 50/30/20 Rule to find what fits your family’s habits and comfort level. The best budget is one you’ll actually use.

4. Regular Reviews and Adjustments

A family budget should evolve as life changes. Revisit it monthly or quarterly to track progress, refine spending categories, and ensure your goals remain relevant. Flexibility keeps the system sustainable.

5. Incorporating Technology

Use budgeting apps and digital tools to automate tracking, categorize expenses, and monitor progress in real time. Tools like YNAB, Mint, or EveryDollar can simplify consistency and communication.

6. Teaching Financial Literacy at Home

Turn budgeting into a lifelong skill by involving children early. Explain spending choices, saving goals, and the value of money in age-appropriate ways—building confidence and healthy financial habits for the next generation.

🔹3. Why Budgeting Matters for Families

A family budget is a plan that tracks household income, expenses, and savings goals to ensure financial stability and long-term success. It helps families manage spending, prepare for emergencies, and work toward shared financial goals.

🔹 What Is a Family Budget?

A family budget is a structured financial plan that tracks your household’s income, expenses, and savings goals. It provides a clear roadmap for how money flows in and out of your household, helping you make informed financial decisions.

At its core, a family budget is designed to:

- Control spending and reduce financial stress

- Prioritize needs and goals over impulse purchases

- Build savings for emergencies and long-term milestones

- Create financial transparency within the household

Unlike individual budgeting, a family budget requires coordination, communication, and shared responsibility. When everyone understands the plan, financial decisions become more intentional—and long-term success becomes more achievable.

🧭 4. Why Learning Personal Finance and Budgeting Is Important for Families

Financial literacy is not just about balancing numbers—it’s about building stability, confidence, and shared responsibility across generations. When families learn about personal finance and budgeting together, they cultivate habits that create lasting security and unity.

1. Strengthening Family Stability

Money is one of the top stressors in relationships. A family that openly discusses and plans finances together reduces tension and avoids last-minute financial crises. Budgeting creates transparency and teamwork, helping everyone pull in the same direction toward shared goals—like paying off debt, saving for college, or planning a vacation.

Key Point: Families who budget together experience lower financial stress and are better prepared for emergencies.

2. Teaching Financial Values to Children

Children learn by observing. When parents model budgeting, saving, and goal-setting, kids internalize those behaviors early. Studies from the University of Cambridge show that children begin forming money habits as early as age 7, meaning early family financial education pays lifelong dividends.

Practical Tip: Involve children in small financial tasks—like comparing prices or saving for a family outing—to make lessons tangible and engaging.

3. Empowering Better Decision-Making

Understanding budgeting empowers every family member to make informed choices. Whether it’s a teen deciding between a used car and public transportation, or parents evaluating mortgage options, financial knowledge leads to more confident, data-driven decisions.

Example: Knowing how interest compounds or how to read a credit report can prevent costly mistakes and build strong financial health.

4. Building Long-Term Wealth and Security

Financial literacy transforms short-term discipline into long-term prosperity. Families who track expenses, plan for retirement, and invest wisely are more likely to achieve financial independence. According to the National Financial Educators Council, adults who received financial education early in life report saving at least $1,200 more annually than those who did not.

Key Point: Budgeting isn’t restrictive—it’s a roadmap to financial freedom.

5. Preparing for Life’s Unexpected Turns

From job loss to medical bills, unexpected events can disrupt even the most stable households. A family versed in budgeting and emergency planning can adapt quickly without falling into debt.

Action Step: Maintain an emergency fund with at least three to six months of expenses and review insurance coverage annually.

✅Takeaway

Learning personal finance as a family transforms money from a source of stress into a shared tool for empowerment. It fosters accountability, strengthens relationships, and lays the groundwork for future generations to thrive financially.

5. Assessing Your Family’s Financial Situation

Before building a budget, you need a clear snapshot of your current financial landscape. This assessment sets the foundation for informed decisions and realistic goals.

Step 1: Gather Financial Information

Collect all relevant financial documents so you can see the full picture of your income, obligations, and spending patterns.

Documents to Review:

- Pay stubs – to determine total monthly income and deductions.

- Bank statements – to track cash flow and recurring expenses.

- Credit card statements – to highlight high-spending categories or potential problem areas.

- Loan documents – to account for mortgages, student loans, car loans, or other debts.

- Investment and savings records – to include interest income, dividends, or retirement contributions.

Step 2: Categorize Your Spending

Once you’ve gathered your information, divide your expenses into categories to understand how money flows through your household.

Expense Categories:

- Fixed Expenses: Predictable monthly costs like rent or mortgage payments, insurance premiums, utilities, and childcare.

- Variable Expenses: Costs that fluctuate, such as groceries, fuel, clothing, and entertainment.

- Discretionary Spending: Non-essential expenses like dining out, subscriptions, and hobbies. These often offer the most flexibility when adjusting your budget.

Step 3: Identify Spending Patterns

Look for trends—are you consistently overspending in certain categories? Do small purchases add up over time? Awareness is the first step toward meaningful change.

Pro Tip: Use a budgeting app or spreadsheet to visualize where your money goes. Seeing percentages rather than dollar amounts can make overspending patterns easier to spot.

⚙️ Next Steps

Once you’ve clarified your financial picture, you’re ready to:

- Set realistic family financial goals that balance short-term enjoyment and long-term security.

- Choose a budgeting method—like zero-based budgeting or the 50/30/20 rule—that fits your family’s lifestyle.

- Engage the whole family in maintaining accountability and celebrating progress together.

6. Setting Realistic Financial Goals

Creating a budget without clear goals is like taking a road trip without a destination. Financial goals give your family’s money purpose and direction, helping you turn everyday decisions into progress toward meaningful outcomes.

Why Goal-Setting Matters

Financial goals transform budgeting from a routine task into a shared mission. They help your family stay motivated, measure success, and make intentional spending decisions. When every dollar is tied to a goal, it becomes easier to say “no” to what doesn’t serve your priorities—and “yes” to what truly matters.

Short-Term Goals (Next 12 Months)

Short-term goals are your quick wins—the small but powerful steps that build financial momentum and confidence.

Examples:

- Build an Emergency Fund: Aim to save three to six months of living expenses to protect against unexpected events like medical bills or job loss.

- Pay Down a Small Debt: Eliminate a credit card balance or personal loan to free up cash flow and boost your credit score.

- Plan a Family Vacation: Save a set amount each month for a trip that celebrates your progress and reinforces the value of delayed gratification.

- Start a Savings Habit: Automate weekly transfers into a high-yield savings account, even if you start small.

Tip: Use the SMART method—set goals that are Specific, Measurable, Achievable, Relevant, and Time-bound. For example, “Save $2,000 for an emergency fund within six months by setting aside $80 per week.”

Long-Term Goals (1–10+ Years)

Long-term goals define your family’s vision for the future. They require planning, patience, and persistence—but they’re the key to lasting financial security.

Examples:

- Save for College: Contribute regularly to a 529 plan or educational savings account to help your children graduate without heavy debt.

- Pay Off the Mortgage Early: Make one extra payment per year or round up your monthly payment to shorten your loan term and build home equity faster.

- Retirement Planning: Maximize contributions to your employer’s retirement plan or IRA to secure financial independence and peace of mind.

- Invest in the Future: Begin or expand an investment portfolio to grow wealth and offset inflation over time.

Tip: Review your goals annually. As your family grows and priorities change, your long-term objectives may evolve. Staying flexible keeps your plan realistic and sustainable.

Involving the Whole Family

A family budget works best when everyone understands why goals matter and feels included in achieving them.

Ways to Get the Family On Board:

- Open Communication: Hold monthly “money meetings” to review progress, celebrate wins, and adjust goals.

- Age-Appropriate Learning: Teach kids how saving, earning, and spending decisions affect the family’s bigger goals. Simple visuals like savings jars or goal charts can make learning fun.

- Shared Decision-Making: Let family members participate in goal-setting. Whether it’s voting on the next vacation spot or choosing a family savings challenge, involvement builds ownership.

- Positive Reinforcement: Celebrate milestones together. Even small achievements—like reaching a savings target—reinforce good habits and teamwork.

💡 Takeaway

Setting realistic financial goals bridges today’s actions with tomorrow’s dreams. It turns budgeting into a family effort rooted in shared purpose, responsibility, and optimism.

Budgeting isn’t just about numbers; it’s about setting a foundation for a stable financial future and teaching valuable life lessons to your children.

7. Creating Your Family Budget

Now that your goals are set and your financial picture is clear, it’s time to design the plan that brings it all together—your family budget. This is where intention meets action, and your financial priorities turn into a practical monthly roadmap.

🔹 How to Create a Family Budget (Quick Steps)

Creating a family budget doesn’t have to be complicated. Follow these five practical steps to build a system that works for your household:

1. Calculate Total Household Income

Add up all sources of income, including salaries, side income, benefits, or irregular earnings. Use your average monthly income if it fluctuates.

2. List All Fixed and Variable Expenses

Break your expenses into categories:

- Fixed expenses: Rent/mortgage, insurance, loan payments

- Variable expenses: Groceries, utilities, gas, entertainment

This helps you understand where your money is going.

3. Set Short- and Long-Term Financial Goals

Define what you’re working toward:

- Short-term: Emergency fund, paying off debt

- Long-term: Retirement, college savings, home upgrades

Clear goals give your budget purpose.

4. Choose a Budgeting Method

Select a structure that fits your lifestyle:

- 50/30/20 Rule: Needs, wants, savings

- Zero-based budgeting: Every dollar has a job

- Envelope system: Cash-based spending control

The best method is the one you can consistently follow.

5. Track and Adjust Monthly

A budget is not “set and forget.” Review it regularly:

- Compare planned vs. actual spending

- Adjust categories as needed

- Stay flexible as life changes

Consistency—not perfection—is what dri

Choosing the Right Budgeting Method

There’s no one-size-fits-all formula for family budgeting. The best approach depends on your household’s spending habits, comfort with tracking, and financial goals. Below are three proven methods families use successfully.

| Budgeting Method | How It Works | Best For | Example |

|---|---|---|---|

| Envelope System | Allocate a set amount of cash to envelopes labeled for categories like groceries, gas, and dining out. Once the envelope is empty, spending stops. | Families who prefer tangible, cash-based control and visual limits. | “Groceries” envelope = $600/month. When empty, no more grocery spending until next month. |

| Zero-Based Budgeting | Every dollar you earn is assigned a purpose—spending, saving, investing, or debt repayment—so that income minus expenses equals zero. | Households aiming for total control and accountability over every dollar. | Monthly income: $5,000 → $5,000 assigned across all categories with $0 left unallocated. |

| 50/30/20 Rule | Divide after-tax income into three simple categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment. | Families seeking a simple, balanced framework without micromanaging. | $6,000 monthly income → $3,000 needs, $1,800 wants, $1,200 savings/debt. |

Tip: Start with one method, track your progress for 2–3 months, and adjust. Many families blend methods—using the 50/30/20 structure for planning and the envelope approach for discretionary spending control.

Allocating Funds

Once you’ve chosen a method, it’s time to assign every dollar a role. Begin with fixed essentials, then work your way toward flexible and aspirational categories.

| Category | Description | Examples |

|---|---|---|

| Fixed Expenses | Non-negotiable monthly obligations. | Mortgage/Rent, Utilities, Insurance, Childcare |

| Variable Expenses | Costs that fluctuate each month. | Groceries, Transportation, Entertainment |

| Discretionary Spending | Non-essential but lifestyle-enhancing items. | Dining Out, Hobbies, Subscriptions |

| Savings & Investments | Money reserved for future goals or security. | Emergency Fund, College Fund, Retirement Accounts |

Balancing Priorities

- Cover the Essentials First: Allocate income to fixed expenses and minimum debt payments.

- Fund Your Goals: Dedicate a set percentage to savings—treat it like a bill that must be paid each month.

- Manage Variable Costs: Use digital tools or a spending tracker to monitor where your money flows.

- Reward Progress: Leave room for small family rewards or experiences—budgeting should support happiness, not restrict it.

Embrace Flexibility

Your family’s needs will evolve—new expenses, income changes, and life milestones are all part of the journey. A successful budget is a living document, not a static rulebook. Review it monthly, adjust categories as needed, and celebrate every improvement.

💡 Pro Tip: Use apps like YNAB (You Need A Budget), Mint, or EveryDollar to automate tracking and sync family accounts. Automation saves time, reduces friction, and keeps everyone accountable.

Sample Family Budget Allocation

| Method | Description | Sample Allocation (Monthly Income: $5,000) |

|---|---|---|

| Envelope System | Cash-based with strict limits per category. | Groceries: $600, Entertainment: $200, Gas: $150, Savings: $1,000 |

| Zero-Based Budgeting | Every dollar assigned to a category. | Needs: $2,500, Wants: $1,200, Savings/Debt: $1,300 |

| 50/30/20 Rule | Simplified balance by percentage. | 50% Needs ($2,500), 30% Wants ($1,500), 20% Savings ($1,000) |

✅ Takeaway

Creating a family budget is about more than tracking expenses—it’s about aligning your money with your values. When done right, it becomes a shared framework for security, communication, and growth.

8.⚠️ Common Family Budget Mistakes to Avoid

Even well-intentioned budgets can fail if key pitfalls are overlooked. Avoid these common mistakes to keep your financial plan on track:

1. Underestimating Variable Expenses

Costs like groceries, utilities, and gas often fluctuate. Underestimating them can quickly throw off your budget.

2. Ignoring Irregular Expenses

Annual or unexpected costs—such as holidays, car repairs, or medical bills—can derail your finances if not planned for.

3. Failing to Review the Budget Regularly

A budget should evolve with your life. Without regular check-ins, it becomes outdated and ineffective.

4. Neglecting Savings Goals

If savings aren’t built into your budget, they often get overlooked. Treat savings like a non-negotiable expense.

💡 Final Insight

A successful family budget isn’t about perfection—it’s about awareness, consistency, and adaptability. By avoiding these common mistakes, you create a system that supports both your current needs and your future goals.

9. Implementing and Maintaining the Budget

Family Meetings and Communication

Regular family meetings are crucial for maintaining your budget. These meetings provide an opportunity to:

- Review Spending: Discuss how the family’s actual spending compares to the budget. This helps identify areas where you’re doing well and aspects that need adjustment.

- Address Changes: Life is dynamic, and so are your finances. Regular meetings allow you to adapt the budget to changes like a salary raise, unexpected expenses, or changing financial goals.

- Foster Inclusion and Accountability: When everyone is involved in the discussions, it fosters a sense of responsibility and collective effort towards maintaining the budget.

Tracking and Monitoring

Effective budget management requires keeping track of income and expenses. There are several tools and methods for this:

- Budgeting Apps: Utilize digital tools and apps to track spending and monitor budget adherence. Many apps can sync with your bank accounts and categorize expenses automatically.

- Spreadsheets: For those who prefer a hands-on approach, a well-organized spreadsheet can be an excellent tool for tracking your budget.

- Receipts and Records: Keeping receipts and financial records organized can be helpful, especially for variable and discretionary expenses.

Dealing with Challenges and Setbacks

It’s normal to face challenges when sticking to a budget. Here’s how to handle them:

- Revisit and Adjust: If you consistently overspend in a category, reassess your budget allocations. It may be necessary to reallocate funds or cut back on certain expenses.

- Emergency Fund: Building an emergency fund can provide a financial cushion and prevent your budget from derailing in unexpected situations.

- Stay Positive: Maintaining a budget can be challenging, but staying positive and focused on your goals is crucial. Celebrate small victories and learn from setbacks.

10. Building Healthy Financial Habits

Consistent Review and Learning

A budget isn’t set in stone; it’s a flexible tool that should evolve with your family’s needs. Consistent review and a willingness to learn and adapt are key. Consider:

- Regular Financial Check-Ins: Schedule monthly or quarterly reviews of your financial situation and budget.

- Continuous Education: Stay informed about financial management practices and educate yourself and your family about financial health.

Table 3: Monthly Family Financial Check-In

| Check-In Item | Purpose | Details/Notes |

|---|---|---|

| Review Spending | Compare actual vs. budgeted spending | Note categories of overspending |

| Assess Savings Goals | Track progress towards savings goals | Adjust contributions if needed |

| Plan for Upcoming Expenses | Anticipate and budget for future expenses | School fees, holiday spending, etc. |

| Adjust Budget as Needed | Keep budget aligned with current needs | Increase/decrease budget categories |

Positive Reinforcement and Rewards

Encouraging good financial behavior within the family is important. Here’s how:

- Celebrate Milestones: Acknowledge when financial goals are met, like paying off a debt or reaching a savings target.

- Reward System: Implement a reward system for sticking to the budget or for good spending decisions, especially for younger family members.

11. Using Technology to Simplify Budgeting

Leveraging Budgeting Apps and Tools

In today’s digital age, numerous tools and apps can simplify and enhance your budgeting process. Here’s how technology can help:

- Automated Tracking: Many apps automatically track and categorize your spending, saving you time and effort.

- Real-Time Updates: Get instant insights into your financial status, helping you make informed decisions on the go.

- Goal Setting Features: Some apps offer features to set and track progress towards your financial goals, keeping you motivated.

Choosing the Right Tool for Your Family

With a plethora of options available, choosing the right tool is crucial. Consider:

- User-Friendliness: The app or tool should be easy to use for all family members.

- Features: Look for features that match your family’s specific needs, such as the ability to sync with your bank accounts, set up multiple user profiles, or provide educational resources.

- Security: Ensure the tool has strong security measures to protect your financial data.

12. Making Budgeting a Family Activity

Making Budgeting a Family Activity

Budgeting doesn’t have to be a chore. Here are some ways to make it fun and engaging for the whole family:

- Budgeting Games: Use games to teach children about money management in a fun and interactive way.

- Family Challenges: Set up friendly competitions, like who can save the most in a month, to encourage saving and mindful spending.

- Rewarding Experiences: Instead of material rewards, consider experiences, like a family outing, as a reward for meeting budgeting goals.

Financial Literacy for Kids

Introducing children to financial concepts early on is vital. You can:

- Age-Appropriate Learning: Use books, online resources, and apps designed to teach children about money in an age-appropriate manner.

- Practical Experience: Give children small amounts of money to manage, like an allowance, to practice budgeting and saving.

13. Handling Financial Challenges and Unexpected Expenses

Anticipating and Planning for the Unexpected

No matter how well you plan, unexpected financial challenges can arise. Here’s how to prepare for them:

- Emergency Fund: Establish and maintain an emergency fund. Aim to save enough to cover at least three to six months of living expenses.

- Insurance: Ensure you have adequate insurance coverage (health, home, auto) to mitigate potential financial losses.

- Flexible Budgeting: Build flexibility into your budget to accommodate unforeseen expenses without derailing your financial goals.

Managing Debt and Reducing Financial Stress

Debt can be a significant source of financial stress for families. Addressing it effectively is crucial:

- Debt Repayment Plan: Prioritize high-interest debts and consider strategies like debt snowball or avalanche methods.

- Seek Professional Advice: If debt becomes overwhelming, consider consulting a financial advisor for personalized guidance.

- Mindful Spending: Continuously evaluate your spending habits to prevent accumulating unnecessary debt.

14. Celebrating Success and Adjusting for the Future

Reflecting on Progress and Achievements

Regularly reflect on your financial journey:

- Review Accomplishments: Take time to acknowledge the progress you’ve made, whether it’s sticking to your budget, reducing debt, or growing your savings.

- Family Discussions: Use these reflections as opportunities for family discussions, reinforcing the value of teamwork in achieving financial goals.

Adjusting Goals and Budget for Future Needs

As your family’s needs and circumstances change, so should your budget:

- Periodic Reassessment: Revisit your financial goals and budget periodically to ensure they align with your current situation and future aspirations.

- Adapting to Life Changes: Be it a new job, a growing family, or planning for retirement, adjust your budget to accommodate these life changes.

🧩 15. Family Budget Example (Step-by-Step Breakdown)

Budgeting becomes much easier once you see how the numbers flow in real life. The following example uses a fictional household, but the process and framework apply to families with a wide range of incomes and circumstances.

This example illustrates how a family turns goals, monthly expenses, and financial priorities into a realistic and sustainable plan—without feeling restricted or overwhelmed.

📘 Meet the Johnson Family

- Parents: Alex and Jordan

- Children: Two (ages 7 and 10)

- Monthly take-home income: $6,800

Primary goals

- Build a $10,000 emergency fund

- Save for kids’ extracurricular activities

- Start planning ahead for family vacations

- Reduce stress around monthly bills and timing

🧭 Step 1 — Calculate Average Monthly Income

After taxes, health insurance, and retirement contributions, Alex and Jordan take home approximately $6,800 per month.

- Paychecks are bi-weekly

- Childcare subsidies already deducted

- Health expenses mostly captured through insurance

🧮 Step 2 — List Regular Monthly Expenses

| Category | Monthly Amount |

|---|---|

| Housing | $2,200 |

| Utilities | $350 |

| Groceries | $800 |

| Transportation | $500 |

| School Supplies/Activities | $250 |

| Internet/Phone | $160 |

| Insurance Premiums | $300 |

| Household Needs | $250 |

| Entertainment | $200 |

| Restaurants/Takeout | $150 |

| Miscellaneous | $190 |

Total regular expenses: $5,350

🧩 Step 3 — Identify Flexible Spending Areas

The Johnsons realized dining out, shopping, and entertainment were driving irregular spending. They created caps based on past habits:

- Eating out → maximum $150/month

- Entertainment → $200/month

- Miscellaneous → $200/month

These numbers are realistic—not restrictive—and still allow room for family enjoyment.

🎯 Step 4 — Assign Savings and Short-Term Goals

After covering essential expenses, the Johnsons allocate the remaining $1,450:

| Purpose | Amount |

|---|---|

| Emergency Fund | $500 |

| Kids’ Activities | $200 |

| Vacation Savings | $300 |

| Home Repairs | $200 |

| Future Car Replacement | $250 |

This creates clear priorities while maintaining flexibility for changing needs.

📊 Johnson Family Monthly Budget Overview

| Category | Amount |

|---|---|

| Income | $6,800 |

| Household Essentials | $5,350 |

| Savings + Goals | $1,450 |

| Balance | $0 (Zero-based design) |

Rather than leaving leftover funds unassigned, they planned every dollar upfront to match monthly priorities.

📆 Step 5 — Add Monthly Review Checkpoints

The family agreed to meet the first Sunday of each month and discuss:

- How spending matched goals

- Whether savings goals need adjusting

- Any upcoming expenses

- Areas for improvement

- Wins worth celebrating

These conversations create participation, ownership, and transparency—especially for kids learning about money.

💡 What the Johnsons Learned

After three months, the Johnsons noticed:

- Restaurant spending dropped by 40%

- Monthly stress decreased

- Kids felt empowered helping choose family goals

- They saved $1,500 in their emergency fund in 90 days

- They communicate more openly about money and priorities

✨ Insights from This Example

- A family budget works best when everyone participates

- Clear spending categories create confidence and teamwork

- Savings goals become achievable when broken into monthly amounts

- Regular check-ins maintain alignment through changing seasons

- Flexibility keeps budgets realistic and sustainable

This example shows how a family can move from reactive spending to proactive planning and shared decision-making—without needing to deprive or sacrifice the things that bring fulfillment and joy.

📆 What This Looks Like in Real Life (Week-by-Week)

Here’s how the Johnson family manages a typical week:

| Category | Weekly Budget | Actual (Week 1) |

|---|---|---|

| Groceries | $200 | $215 |

| Gas | $125 | $110 |

| Dining Out | $35 | $50 |

| Miscellaneous | $50 | $40 |

👉 Result:

- Over budget by $15 overall

Adjustment:

- Reduce dining out next week

- Shift $15 from miscellaneous buffer

16. ⚡ Simple Family Budget You Can Copy Today

If you want to skip the setup and get started immediately, use this simplified version:

| Step | Action |

|---|---|

| 1 | Write down total monthly income |

| 2 | List your top 5 fixed expenses |

| 3 | Set 3 weekly spending limits (groceries, gas, discretionary) |

| 4 | Choose 1 savings goal |

| 5 | Review every Sunday for 10 minutes |

17. 🧠What Would YOU Do? (Quick Decision Check)

Budgeting isn’t just about numbers—it’s about decisions in real time.

🤔 Quick Decision Check

If you were in the Johnson family’s position and went over budget this week, what would you do?

- Cut back next week

- Pull from savings

- Ignore it and adjust monthly

- Increase income temporarily

👉 There’s no perfect answer—but the key is making a conscious, intentional decision.

Every option has trade-offs:

- Cutting back builds discipline

- Using savings protects consistency but slows long-term goals

- Ignoring it can create patterns if repeated

- Increasing income adds flexibility but requires time and effort

👉 The goal isn’t perfection—it’s awareness and control.

🎯 Why This Matters

Making small, intentional adjustments each week helps you:

- Stay aligned with your financial goals

- Prevent small overspending from becoming long-term issues

- Build confidence in managing money as a family

18. 📌 Common Family Budget Mistakes to Avoid

Even the best budget can fall apart if a few key pitfalls are overlooked. Watch for these common mistakes:

⚠️ Where Families Go Wrong

- Setting unrealistic spending limits

→ Overly strict budgets often lead to frustration and burnout - Forgetting irregular expenses (birthdays, holidays, car repairs)

→ These “surprise” costs can derail an otherwise solid plan - Not reviewing the budget regularly

→ Without check-ins, small issues go unnoticed until they grow - Treating the budget as rigid instead of flexible

→ Life changes—your budget should adapt with it - Leaving “extra money” unassigned

→ Unplanned money often gets spent unintentionally

💡 Simple Fix

👉 Fixing just one of these can dramatically improve your results.

Start small:

- Add a monthly “miscellaneous buffer”

- Schedule a 10-minute weekly review

- Adjust categories based on real spending—not guesses

🚀 Pro Tip

A successful family budget isn’t about getting everything right the first time—it’s about making small, consistent improvements over time.

💬 19. Frequently Asked Questions (FAQs)

1. How do I start a family budget if I’ve never had one before?

Start simple. Gather your financial information—income, expenses, and debts—then track your spending for one month to identify patterns. Once you see where your money goes, set clear financial goals and choose a budgeting method (like the 50/30/20 rule or zero-based budgeting). Focus on progress, not perfection—the key is to get started.

2. What if my expenses are higher than my income?

This is a common challenge. Begin by reviewing your discretionary spending (eating out, subscriptions, entertainment) and find areas to cut back. Look for opportunities to reduce fixed costs—like refinancing a loan or negotiating insurance rates—and explore ways to increase income, such as part-time work or freelancing. If financial stress persists, consider consulting a Certified Financial Planner™ or nonprofit credit counselor for guidance.

3. How can I make budgeting a family activity?

Turn budgeting into teamwork. Hold monthly “family money meetings” where everyone—kids included—shares updates and ideas. Use visuals like goal charts or savings jars to make progress tangible. Celebrate milestones together (like paying off a debt or reaching a savings target) to keep motivation high.

4. How often should we review or update our budget?

At least once every three months, or anytime your financial situation changes—such as a new job, a large purchase, or a shift in expenses. Regular reviews help you stay proactive instead of reactive, adjusting before small issues become bigger ones.

5. What’s the easiest way to track spending and stay on budget?

Choose a system that fits your lifestyle.

- Digital Apps: Tools like YNAB, Mint, or EveryDollar automate tracking and categorize expenses.

- Spreadsheets: Great for visual learners who prefer custom layouts.

- Manual Tracking: Pen and paper can work well for those who prefer hands-on engagement.

Consistency matters more than method—pick one and stick with it.

6. How can we save money while living on a tight budget?

Start by prioritizing necessities and identifying non-essentials to trim. Use strategies like:

- Buying in bulk for staples.

- Using cash-back or coupon apps.

- Cooking at home instead of dining out.

- Cutting unused subscriptions or memberships.

Even saving $20 a week adds up to over $1,000 a year—small steps make a big difference.

7. What’s the best way to teach kids about money and budgeting?

Involve them early. Give children hands-on experiences with money through:

- Allowances tied to chores.

- Savings goals for something they want to buy.

- Games and simulations that make budgeting fun (like setting up a “family store” or using educational apps).

The goal is to make money management feel empowering—not restrictive.

💡 Final Thought

Family budgeting isn’t just about managing money—it’s about strengthening communication, teaching responsibility, and creating a shared vision for your financial future. When the whole family participates, budgeting becomes a tool for unity and confidence.

20. Family Budget Checklist

1. Initial Assessment and Setup

- Gather all financial documents (pay stubs, bank statements, bills, etc.).

- Track and categorize all expenses for at least one month to understand spending habits.

- List all income sources, including regular and occasional earnings.

- Identify and list all fixed, variable, and discretionary expenses.

- Discuss financial goals and priorities as a family.

2. Setting Financial Goals

- Define short-term financial goals (e.g., saving for a family vacation).

- Establish long-term financial goals (e.g., saving for retirement, children’s education).

- Agree on a timeline for achieving these goals.

- Determine monthly savings needed to meet each goal.

3. Choosing a Budgeting Method

- Research and understand different budgeting methods (envelope system, zero-based budgeting, etc.).

- Select a budgeting method that aligns with your family’s financial situation and goals.

- Create categories for all expenses based on the chosen method.

4. Allocating Funds

- Allocate income to different expenses starting with fixed and essential expenses.

- Set aside funds for savings goals.

- Distribute remaining funds to variable and discretionary expenses.

- Ensure a portion of income is allocated for emergency funds.

5. Implementing the Budget

- Communicate the budget plan to all family members.

- Use budgeting tools or apps for tracking income and expenses.

- Schedule regular family meetings to review the budget.

- Keep receipts and financial records organized for tracking.

6. Monitoring and Adjusting the Budget

- Track spending and compare it against the budget regularly.

- Adjust budget allocations as needed based on actual spending.

- Revisit financial goals periodically and adjust the budget accordingly.

- Review and adjust the budget for any significant life changes (e.g., new job, new family member).

7. Building and Maintaining Financial Discipline

- Encourage all family members to share ideas for cost savings.

- Reward family members for sticking to the budget or making smart financial choices.

- Educate children about financial responsibility and involve them in budget-related activities.

- Continuously seek ways to improve financial knowledge and skills.

8. Reviewing and Celebrating Success

- Regularly reflect on and acknowledge progress made towards financial goals.

- Celebrate achieving milestones (e.g., paying off debt, reaching savings targets).

- Adjust future goals based on past successes and challenges.

21. Family Budget Template

1. Monthly Income

| Source | Amount ($) |

|---|---|

| Salary 1 | 3,000 |

| Salary 2 | 2,500 |

| Part-Time Job | 500 |

| Other Income | 200 |

| Total Income | 6,200 |

2. Fixed Expenses

| Category | Amount ($) |

|---|---|

| Mortgage/Rent | 1,200 |

| Utilities (Electric, Gas, Water) | 300 |

| Insurance (Health, Auto) | 400 |

| Internet/Phone | 150 |

| Total Fixed Expenses | 2,050 |

3. Variable Expenses

| Category | Amount ($) |

|---|---|

| Groceries | 600 |

| Gas/Transportation | 250 |

| School Expenses | 200 |

| Total Variable Expenses | 1,050 |

4. Discretionary Spending

| Category | Amount ($) |

|---|---|

| Dining Out | 150 |

| Entertainment | 100 |

| Hobbies | 75 |

| Miscellaneous | 50 |

| Total Discretionary Spending | 375 |

5. Savings & Investments

| Goal | Amount ($) |

|---|---|

| Emergency Fund | 300 |

| Retirement Savings | 400 |

| College Fund | 200 |

| Total Savings & Investments | 900 |

6. Total Expenses and Savings

| Category | Amount ($) |

|---|---|

| Total Fixed Expenses | 2,050 |

| Total Variable Expenses | 1,050 |

| Total Discretionary Spending | 375 |

| Total Savings & Investments | 900 |

| Total Expenses and Savings | 4,375 |

7. Monthly Surplus/Deficit

| Description | Amount ($) |

|---|---|

| Total Income | 6,200 |

| Total Expenses and Savings | 4,375 |

| Surplus/Deficit | 1,825 |

Budget Analysis

This section of the budget reflects that the family has a surplus of $1,825 this month, which can be allocated to additional savings, debt repayment, or future large purchases. Regular review and adjustment of the budget are crucial as income and expenses change.

This template can be customized to fit the specific needs of your family. For example, you might have different categories under fixed, variable, and discretionary spending, or you might want to allocate more towards savings or specific goals. You can also adapt it for use in a spreadsheet program like Microsoft Excel or Google Sheets to make calculations automatic and tracking easier.

Go Check out our budgeting template at:

Comprehensive Family Budgeting Template Link to Template

🏁 Conclusion – Empowering Your Family’s Financial Future

Key Steps to Building a Budget That Works

Let’s recap the essential building blocks of a successful family budget:

- Assess Your Financial Situation: Gather your income, expenses, and debt details to understand where your money is going.

- Set Clear Financial Goals: Define both short-term and long-term objectives that align with your family’s priorities.

- Create the Budget: Choose a budgeting method that fits your lifestyle and allocate funds intentionally across needs, wants, and savings.

- Implement and Maintain It: Track spending, hold family budget meetings, and use digital tools to stay organized and accountable.

- Navigate Challenges: Expect financial surprises—build an emergency fund, manage debt proactively, and stay flexible.

- Celebrate and Adjust: Recognize progress, celebrate milestones, and update your plan as your family’s life evolves.

The Power of a Family Budget

A thoughtful, well-structured budget is more than a financial plan—it’s a framework for family growth and stability. It:

- Brings clarity to spending and priorities.

- Promotes teamwork and communication between family members.

- Encourages financial discipline while allowing room for joy and spontaneity.

- Builds confidence by transforming financial stress into measurable progress.

Families who budget together create a shared sense of purpose—one that extends beyond dollars and cents to values, goals, and future opportunities.

Take Action Today

The best time to start taking control of your family’s financial future is right now.

Sit down together, open the conversation, and begin designing a plan that reflects your shared goals and values.

Use the resources and templates in this guide to:

✅ Build your first budget.

✅ Choose a system that works for your lifestyle.

✅ Empower every family member to play a role in your collective success.

Remember—budgeting isn’t about restriction; it’s about direction. The journey to financial peace begins with one simple step: start planning together today.

🔗 Continue Your Financial Learning

Take the next step in building a stronger financial foundation with these structured guides:

🧭 Budgeting & Money Management Hub

Explore proven strategies, tools, and frameworks to manage your money more effectively.

→ Explore Budgeting

🧠 Jason’s Fin Tips Budgeting Frameworks

Learn how to choose and implement a budgeting system that fits your lifestyle and financial goals.

→ Learn About Budgeting Frameworks

Tax Planning & Optimization

Understand how tax systems work and apply strategies that reduce surprises and improve financial efficiency.

→ Explore the Tax Hub

🎯 How to Create a Financial Plan

Turn your budget into a complete financial strategy with clear goals and long-term direction.

→ Step-by-Step Planning Guide

Back to Creating A Budget

Explore the Finance Hub