🏦 1. Introduction

Have you ever opened your bank statement and felt like you’re reading a foreign language? You’re not alone. Between transaction codes, acronyms, and endless lines of figures, a simple statement can feel more like a puzzle than a financial snapshot.

Yet within those numbers lies a powerful story — one that reveals how you earn, spend, save, and manage your money. Learning to interpret your bank statement isn’t just about identifying charges; it’s about understanding your financial behavior and using that insight to make smarter choices.

In this guide, we’ll decode your bank statement step-by-step. You’ll learn:

- How to interpret key sections and common banking terms.

- What hidden patterns say about your habits.

- Tools and automations to simplify the review process.

- How your statement reflects your overall financial health.

- Action steps to turn insight into measurable progress.

Whether you’re building financial literacy, running a creator business, or just trying to stay organized, this article will help you turn your bank statement from a confusing document into a practical roadmap for better money management.

🧭 2. Key Takeaways

- Bank Statements as Financial Dashboards

View your bank statement as more than a list of transactions — it’s a real-time snapshot of your financial health, spending patterns, and cash flow trends. - Empowerment through Understanding

Decoding each section and term builds financial confidence, helping you make informed decisions about saving, spending, and goal setting. - Proactive Money Management

Use the insights from your statements to create budgets, automate savings, eliminate recurring leaks, and strengthen your long-term financial plan. - Technology as a Financial Ally

Automate alerts, use budgeting apps, and link secure tools to simplify your reviews, catch errors faster, and make financial tracking effortless. - Vigilance against Errors and Fraud

Regularly reviewing your statements helps you spot unauthorized charges early, avoid overdrafts, and protect your financial accounts from misuse. - Growth Mindset and Continuous Learning

Treat every statement review as a learning opportunity — refine habits, identify progress, and stay engaged with your evolving financial goals.

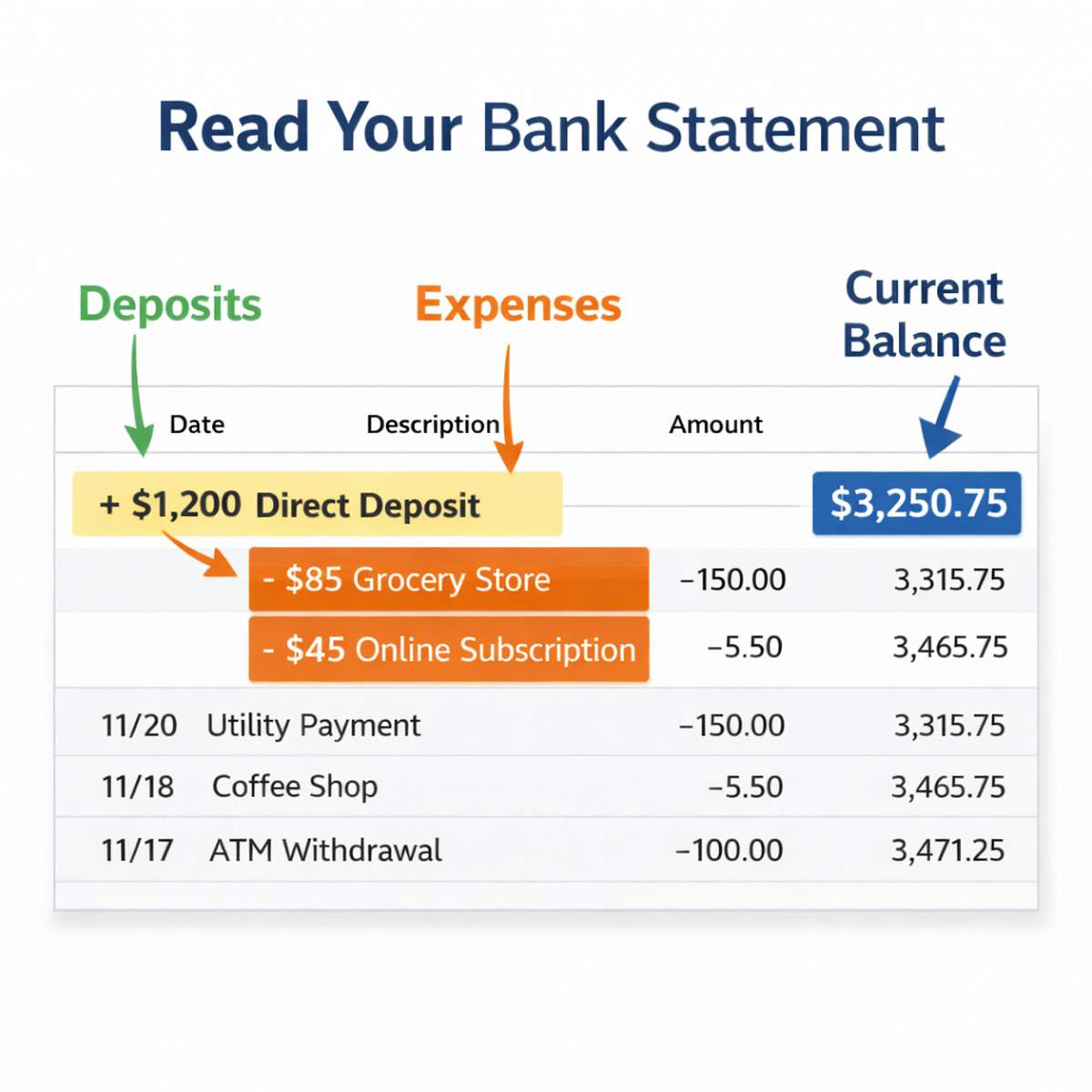

3. Understanding the Basic Components of a Bank Statement

- Account Summary: This section provides a snapshot of your account, including the opening and closing balance for the statement period. It’s a quick way to see if your account is where you expect it to be.

- Example: If your opening balance is $1,000 and your closing balance is $800, it means there was more outgoing than incoming money during the period.

- Deposit Summary: Here, you’ll find a list of all the credits to your account. This includes your income, transfers in, and any other money deposited into your account.

- Example: Look for your salary, which should appear as a regular entry if you have a steady job.

- Withdrawal Summary: This part details money going out of your account, such as payments, ATM withdrawals, and transfers.

- Example: Regular payments like rent or subscription services will show up here.

Deciphering Common Terms and Abbreviations

- ATM: Automated Teller Machine transaction.

- DD: Direct Debit, a pre-authorized withdrawal for bills.

- CR: Credit, an increase in your account.

- DR: Debit, a decrease in your account.

Table 1: Common Terms and Abbreviations in Bank Statements

| Term/Abbreviation | Meaning |

|---|---|

| ATM | Automated Teller Machine transaction |

| DD | Direct Debit, a pre-authorized withdrawal |

| CR | Credit, an increase in your account |

| DR | Debit, a decrease in your account |

| BAL | Balance, the amount of money in your account |

| OD | Overdraft, when spending exceeds the balance |

4. Understanding the “Deposit Summary” Section of Your Bank Statement

What is the Deposit Summary?

The Deposit Summary section of your bank statement provides a detailed list of all credits added to your account during the statement period. These credits could include your salary, any transfers received, refunds processed, and other types of deposits. This section is critical for verifying that you have received all expected funds and for tracking the sources of your income.

Key Components to Look For

- Total Deposits: This figure represents the total amount of money credited to your account during the statement period. It helps you see at a glance whether your expected income matches the actual credits received.

- Individual Entries: Each deposit will be listed individually with details including the date of the deposit, the source or description of the transaction, and the amount. For example, your paycheck might show up as ‘Direct Deposit – ABC Corp.’

- Fees Reversed: Sometimes, this section also includes reversals of certain charges, such as bank fees or penalties that were credited back to your account.

How to Use This Information

- Verify Your Income: Check each entry to confirm that you received your expected income, such as your salary or any other regular payments. Ensure there are no discrepancies in the amounts.

- Identify Unexpected Credits: Look for any deposits that you do not recognize or were not expecting. These could be errors, or in some cases, could alert you to unauthorized activity.

- Financial Planning: Use the total deposits figure to help plan your budget and financial strategy. Knowing exactly how much money is coming in can help you make more informed decisions about spending, saving, and investing.

Example Walk-Through

Suppose your Deposit Summary shows the following entries for the month:

- Direct Deposit – ABC Corp: $2,500

- Mobile Deposit – Check #1234: $150

- ATM Deposit: $200

- Refund – Online Shopping XYZ: $45

Total Deposits: $2,895

From this example, you can confirm your salary deposit from ABC Corp, recognize a check you deposited via your mobile app, note a cash deposit made at an ATM, and identify a refund received from an online shopping return.

Why It’s Important

Understanding the Deposit Summary allows you to confirm that all your expected funds have arrived and alerts you to any unusual or unexpected credits. Regularly monitoring this section helps maintain a healthy financial status and ensures that your financial records are accurate and up-to-date.

5. Analyzing Transactions for Better Financial Planning

Understanding how money flows in and out of your account is crucial for sound financial management. By categorizing transactions on your bank statements, you can gain valuable insights into your spending habits and make informed decisions about budgeting and saving. Let’s explore how to analyze these transactions effectively.

- Categorizing Transactions

- Necessities: These are expenses essential for daily living, such as groceries, utilities, and rent or mortgage payments.

- Tip: Track these costs to ensure they align with your budget expectations.

- Luxuries: Non-essential expenditures, like dining out, entertainment, and shopping for non-essentials.

- Advice: Consider if these can be reduced to save money.

- Recurring Payments: Regular payments such as subscriptions, insurance premiums, or loan repayments.

- Strategy: Review these regularly to see if any can be eliminated or reduced.

- Necessities: These are expenses essential for daily living, such as groceries, utilities, and rent or mortgage payments.

- Identifying Spending Patterns

- Analyze your financial statement to spot trends in your spending. For example, are there certain times of the month when your spending spikes?

- Look for areas where you can cut back. Small changes can add up to significant savings over time.

- Setting a Budget

- Use the information from your bank statement to set a realistic budget.

- Allocate amounts for different categories and stick to them. Adjust as needed based on your spending analysis.

- Saving for the Future

- Identify areas of excess spending to redirect funds towards savings or investment.

- Consider setting up automatic transfers to a savings account right after payday.

- Identifying Discrepancies or Unusual Activities

- Regularly check your statements for any unauthorized transactions or errors.

- Report any suspicious activity to your bank immediately.

- Making Adjustments for Financial Goals

- Based on your transaction analysis, adjust your spending habits to align with your short-term and long-term financial goals.

- This may include increasing savings, strategies to reduce debt, or allocating funds towards investments.

By taking the time to analyze the transactions on your bank statements, you can make more informed decisions about your finances. This process helps you identify areas where you can save, areas where you may be overspending, and opportunities to realign your spending with your financial goals. With this knowledge, you’re better equipped to take control of your financial future.

6. Spotting Red Flags and Avoiding Fees

Being vigilant about the details in your bank statement can not only help you manage your finances better but also protect you from fraud and unnecessary charges. Let’s explore how to spot red flags and avoid fees:

- Spotting Red Flags

- Unrecognized Transactions: Look for purchases or withdrawals you don’t recall making. These could be signs of fraudulent activity.

- Duplicate Charges: Sometimes, merchants may accidentally charge you twice. Keep an eye out for this error.

- Sudden Changes in Account Balance: Large, unexplained changes in your balance should be investigated immediately.

- Unfamiliar Vendor Names: Sometimes, companies have different billing names. If you don’t recognize a vendor, investigate further.

- Regular Review and Reconciliation

- Make it a habit to review your bank statement monthly.

- Match your receipts with the transactions listed to ensure accuracy.

- Avoiding Fees

- Overdraft Fees: Keep track of your balance to avoid overdrawing your account. Consider setting up account alerts to notify you when your balance is low.

- ATM Fees: Use ATMs within your bank’s network to avoid fees. Plan withdrawals to reduce the frequency of ATM use.

- Monthly Maintenance Fees: Some banks charge a fee if your balance falls below a certain amount. Keep your balance above this threshold or consider switching to a bank with no maintenance fees.

- Disputing Errors

- Contact your bank immediately if you spot an error or fraudulent transaction.

- Keep records of your communication for future reference.

- Understanding Fee Structures

- Review the fee structure of your bank account. Be aware of any transaction limits or conditions that may trigger fees.

- Negotiating with Your Bank

- If you face a fee for the first time, you may be able to get it waived by contacting your bank.

- Building a good relationship with your bank can also lead to more favorable terms over time.

Table 2: Types of Banking Fees and Avoidance Strategies

| Type of Fee | Explanation | Avoidance Strategy |

|---|---|---|

| Overdraft Fee | Charged when spending exceeds account balance | Monitor account balance, set up alerts |

| ATM Fee | Charged for using ATMs outside your bank’s network | Use in-network ATMs, plan withdrawals |

| Monthly Maintenance Fee | Charged for account upkeep below a certain balance | Maintain minimum balance, consider no-fee accounts |

| Foreign Transaction Fee | Charged for transactions in foreign currencies | Use credit cards with no foreign transaction fees |

| Returned Item Fee | Charged for bounced checks or failed payments | Ensure sufficient funds before issuing checks or payments |

Staying vigilant about your bank statement is crucial for maintaining financial health. By spotting red flags promptly and understanding how to avoid fees, you can save money and prevent potential fraud. Regularly reviewing your statement and knowing your bank’s fee structure are key practices in effective financial management.

Have you ever spotted a discrepancy on your bank statement? How did you handle it?

📘 7. Common Bank Statement Terms & Misclassifications Explained

Bank statements are full of abbreviations and coded terms that can make even financially savvy readers pause. Decoding them is essential to avoid confusion — or worse, missing unauthorized activity.

🏦 Common Statement Terms Demystified

| Term | What It Means | Why It Matters |

|---|---|---|

| ACH Debit | A payment pulled from your account by another party (e.g., subscription, bill pay). | Review regularly — errors or fraud often appear here first. |

| ACH Credit | Funds pushed into your account (e.g., direct deposit, refund). | Always confirm the source and expected amount. |

| Pending Transaction | A transaction authorized but not yet finalized. | May change or drop off — check back before disputing. |

| POS (Point of Sale) | Purchase made with your debit card in person. | Helps identify where your money is being spent. |

| EFT (Electronic Funds Transfer) | Any digital money transfer between accounts. | Track these to understand digital cash flow patterns. |

| Overdraft Fee | A penalty for spending more than your balance. | Repeated fees are red flags — consider overdraft protection or budgeting adjustments. |

| NSF (Non-Sufficient Funds) | A failed payment due to lack of funds. | Can hurt your credit or lead to bank account closure if repeated. |

⚠️ Frequent Misclassifications to Watch For

- Duplicate or Phantom Charges:

Temporary holds (e.g., gas stations, hotels) may appear as charges and disappear once the final transaction posts. - Third-Party Processor Names:

Some purchases list the payment processor instead of the merchant (e.g., Stripe, Square, or PayPal). Use context clues like timing and amount. - Grouped Merchant Codes:

Some banks consolidate small retailers under one code — you may need to cross-reference your receipts. - Abbreviations or Truncated Names:

For example, “WM SUPCTR 2548” = Walmart Supercenter, store #2548.

✅ Tip

If you ever see a charge you don’t recognize:

- Check the date and location.

- Search the transaction code online — many processors publish lookup databases.

- Call your bank’s fraud department immediately if the source remains unclear.

Even a single unverified charge could indicate card compromise or billing errors.

🧩8. How to Read Between the Lines – Spotting Hidden Spending Patterns

Your bank statement isn’t just a record of transactions — it’s a behavioral mirror. The numbers tell a story about your habits, priorities, and financial blind spots. Learning to “read between the lines” can help you identify silent leaks in your budget long before they become real problems.

🔍 Look for These Red Flags

- Recurring Small Charges:

Those $5–$15 subscriptions add up. Streaming services, app renewals, and memberships can easily total hundreds of dollars a year.

→ Tip: Review all “recurring” or “automatic” payments quarterly and cancel those you rarely use. - Post-Paycheck Spending Surges:

If your account balance drops sharply after payday, it may signal impulse spending or a lack of automation for savings.

→ Tip: Set up an automatic transfer to savings right after payday — pay yourself first. - ATM or Convenience Fees:

Frequent ATM fees often mean you’re withdrawing cash without a plan.

→ Tip: Use your bank’s mobile locator to find fee-free ATMs or withdraw in larger, less frequent amounts. - Irregular Expense Clusters:

Large groups of purchases (like multiple restaurant or delivery charges) in short time frames often reveal “spending moods.”

→ Tip: Create alerts that notify you when your dining or entertainment spending exceeds your budgeted limit.

💡 Turn Insights into Action

- Download the past three months of statements.

- Highlight repeating charges and categorize them (subscriptions, entertainment, household).

- Identify “seasonal” or one-off spikes that you can plan for next time (e.g., holiday gifts, school supplies).

- Summarize total recurring expenses to see how much of your income is “pre-spent” each month.

Goal: Transform awareness into control — your spending habits should align with your values, not surprise you at month-end.

📊 9. What Your Bank Statement Reveals About Your Financial Health

A bank statement isn’t just a list of numbers — it’s a financial diagnostic report. When you know what to look for, you can use it to assess your cash flow, spending habits, and long-term progress.

💵 1. Your Cash Flow Story

Look at the pattern of deposits versus withdrawals over several months.

- Positive cash flow (more deposits than withdrawals) = healthy financial momentum.

- Negative cash flow = risk of debt dependence or poor budgeting.

Quick check: If your average daily balance trends downward month after month, it’s time to adjust spending or increase savings contributions.

📈 2. The 50/30/20 Benchmark

Use your statement to calculate spending ratios:

- 50% Needs (housing, utilities, groceries)

- 30% Wants (entertainment, dining)

- 20% Savings & Debt Repayment

Action Step: Add up the totals from your last statement and compare — if “wants” exceed 30%, plan small reductions next month.

📉 3. Spotting Hidden Financial Leaks

Bank statements often expose silent drains:

- Multiple overlapping subscriptions

- Frequent ATM fees or overdrafts

- Unused memberships or auto-renewals

Over a year, even $25/month in unused services equals $300 lost — enough to boost an emergency fund or pay a credit card bill early.

🧩 4. Understanding Behavioral Patterns

Your spending timeline tells you more than totals:

- Weekend spikes → impulse or social spending

- End-of-month gaps → cash-flow stress

- Mid-month deposits → side hustle or irregular income management

Track these to anticipate when financial pressure builds and plan buffer savings.

🛡️ 5. Long-Term Financial Indicators

Use your statements to monitor improvement over time:

- Declining frequency of overdrafts or late fees

- Growing average daily balance

- Increasing number of automatic savings transfers

- Reduced discretionary spending percentage

If those metrics trend positively, your financial health is improving — even if income hasn’t changed.

🔑 Takeaway

Your bank statement is more than paperwork — it’s a personal financial dashboard.

By learning to interpret it like a pro, you transform it from a record of the past into a tool for planning your future.

10. Using Your Bank Statement to Improve Financial Health

Your bank statement is more than just a record of transactions; it’s a tool that can help you build a stronger financial future. By analyzing the data in your bank statements, you can identify spending patterns, understanding bank fees, set realistic budgets, and work towards your financial goals.

- Creating a Budget Based on Historical Data

- Review past bank statements to understand your average monthly expenses.

- Categorize expenses to identify areas where you can potentially cut back.

- Set a budget for each category and track future spending against these limits.

- Building an Emergency Fund

- Use insights from your bank statements to determine how much you can save each month.

- Aim to build an emergency fund with a strategy that covers 3-6 months of living expenses.

- Consider setting up automatic transfers to a savings account to ensure consistent savings.

- Analyzing Income and Expenses for Debt Reduction

- Compare your monthly income to your expenses. Use any surplus to pay down debts, starting with high-interest debts first.

- Identify non-essential expenses that can be reduced to allocate more towards debt repayment.

- Planning for Long-Term Savings Goals

- Set specific, measurable savings goals such as retirement, a child’s education, or a home purchase.

- Determine how much you need to save each month to meet these goals and monitor your progress.

- Improving Credit Score

- Ensure timely payment of bills and credit card charges, as reflected in your statement, to improve your credit score.

- Keep credit utilization low and avoid opening new lines of credit unnecessarily.

- Investment Opportunities

- With a clear understanding of your financial situation, explore investment options suitable for your risk profile and long-term objectives.

- Consider consulting with a financial advisor to make informed investment decisions.

Effectively utilizing the information in your bank statements can significantly contribute to improving your financial health. By setting budgets, saving for emergencies, reducing debt, and planning for the future, you can take control of your finances and work towards achieving your financial goals.

⚙️ 11. Tools & Automations to Make Bank Statement Reviews Easier

Manually reviewing your bank statement each month can be tedious — but automation makes it simple, accurate, and consistent. With the right tools, you can catch errors early, track progress toward goals, and stay informed without hours of manual work.

💻 Leverage Your Bank’s Built-In Tools

Most modern banks offer digital tools that go far beyond just showing transactions:

- Spending Categories & Pie Charts:

Many online banking dashboards automatically group expenses (e.g., groceries, dining, entertainment). Use this feature monthly to see where your money really goes. - Automatic Alerts:

Set push notifications for:- Purchases over a set amount (e.g., $100+)

- Low-balance warnings

- Recurring charges

- Deposits posted

→ This helps prevent overdrafts and keeps you informed instantly.

- Customizable Budget Goals:

Some banks let you set spending limits or monthly savings targets. Track your progress directly from your app.

📱 Connect to Personal Finance Apps

Integrate your accounts with trusted third-party tools (securely, using read-only access):

| App | Best For | Highlights |

|---|---|---|

| Mint / Credit Karma Money | Everyday budgeting | Auto-categorizes expenses, flags trends |

| You Need a Budget (YNAB) | Zero-based budgeting | Assign every dollar a purpose |

| Rocket Money / Truebill | Subscription management | Detects and cancels unused subscriptions |

| Empower (formerly Personal Capital) | Tracking net worth | Combines banking + investment insights |

| Google Sheets Budget Template | DIY users | Customizable, private, exportable |

💡 Always review privacy settings — ensure apps have “read-only” connections and don’t share your data with third parties.

🧠 Automate Smarter Habits

Use your statement data to set up automations that align with your goals:

- Automatic Transfers to Savings: Move a set percentage of each deposit into your savings account immediately.

- Round-Up Savings Programs: Some banks round purchases to the nearest dollar and deposit the difference into savings.

- Credit Card Payment Alerts: Get notified a few days before due dates to avoid late fees.

- End-of-Month Snapshot: Create a recurring reminder (Google Calendar or Notion) to review your statement for anomalies or trends.

Goal: Let technology handle the monitoring — you focus on decision-making.

🗓️ 12. From Understanding to Action – The 30-Day Bank Statement Challenge

Knowing what your statement says is only half the job — using that information to change behavior is where financial progress begins. This 30-day challenge turns passive awareness into active money management.

🔧 Week 1 – Gather & Organize

- Download the last three months of bank and credit-card statements.

- Label recurring charges, income deposits, and one-time expenses with color codes (e.g., yellow = income, red = fees).

- Identify at least three automatic payments you can review or renegotiate (subscriptions, utilities, or insurance).

💡 Week 2 – Spot Patterns & Leaks

- Total your recurring non-essential charges.

- Highlight any fees (overdrafts, late payments, ATM).

- Ask yourself: “Did I get full value from this expense?”

- Create a “Stop-Doing” list for services or habits you plan to cut.

💰 Week 3 – Reallocate & Automate

- Redirect canceled-subscription money into savings or debt repayment.

- Set an automatic transfer (even $25 per paycheck) to an emergency fund.

- Establish account alerts for low balances or large transactions.

🚀 Week 4 – Review Progress & Plan Ahead

- Compare spending before and after your changes.

- Track total savings recovered — even small wins build momentum.

- Add the review as a monthly calendar reminder so it becomes habit.

Challenge Goal:

Within 30 days, reduce unnecessary spending by 10 % and redirect that money toward savings or debt reduction.

🎨13. Special Considerations for Creators & Irregular Income Earners

For freelancers, influencers, or gig-based professionals, bank statements reveal not only spending patterns but also income volatility. Understanding those fluctuations is key to staying stable between pay cycles.

💼 1. Track Income Like a Business

- Separate personal and business accounts.

- Tag deposits by project, client, or platform (e.g., YouTube AdSense, OnlyFans, affiliate payments).

- Use that data to build a monthly revenue average — critical for tax prep and budgeting consistency.

🧾 2. Smooth Out Volatile Cash Flow

- During high-earning months, transfer 20–30 % of net income into a “buffer” account.

- During lean months, draw from that buffer rather than using credit.

- Treat your average three-month income as your working salary for predictable budgeting.

🪙 3. Match Expenses to Revenue Cycles

- Align major expenses (software renewals, equipment purchases, insurance premiums) with peak-income months.

- Automate minimum savings and tax transfers immediately after each payout.

Pro Tip: Use your statement data to calculate your “burn rate” — how much cash you spend monthly when business is slow. Knowing that number lets you size your emergency fund realistically.

📊 4. Analyze Performance Trends

Export statement data quarterly to a spreadsheet. Track:

- Total monthly deposits

- Total monthly expenses

- Profit margin (net income ÷ gross income)

- Ratio of personal draws to reinvestment

These insights show whether your creator business is scaling sustainably or overspending as revenue rises.

🧠 5. Plan for Taxes & Retirement

- Dedicate 25–30 % of income to a tax savings account.

- Use IRA or Solo 401(k) contributions to reduce taxable income.

- Note recurring tax-deductible charges (e.g., subscriptions, internet, gear purchases) for year-end reporting.

🎯 Key Takeaway

For creators and freelancers, the bank statement is both a report card and a forecasting tool.

Treat it like a business ledger: analyze patterns, automate reserves, and let the data guide smarter decisions.

🧩 14. Example Scenario- How to Read a Bank Statement Step-by-Step

Sometimes the best way to understand a bank statement is to look at a real example. Imagine you’re reviewing your monthly statement and you see the following transactions listed. Here’s what each line can tell you about your financial habits and cash flow.

🔍 Sample Transaction Snapshot

| Date | Description | Amount | Type |

|---|---|---|---|

| 05/03 | Payroll Deposit | +$2,150.00 | Deposit |

| 05/05 | Grocery Store | –$126.45 | POS Debit |

| 05/06 | Netflix Subscription | –$15.49 | ACH Debit |

| 05/07 | ATM Fee | –$3.50 | Service Fee |

| 05/11 | Utility Payment | –$92.18 | ACH Debit |

| 05/13 | Interest Earned | +$0.86 | Interest |

| 05/15 | Out-of-Network ATM | –$60.00 | Withdrawal |

🧠 What These Lines Reveal

🔹 1. Cash-In and Income Timing

Your paycheck arrives on the 3rd, meaning bills scheduled before that date could risk overdraft unless you have a buffer. Knowing your deposit rhythm helps you time expenses.

🔹 2. Everyday Spending Adds Context

Grocery spending is a normal household expense, but tracking it month-to-month helps you identify rising prices or overspending trends.

🔹 3. Recurring Charges Add Up

Subscriptions (Netflix, streaming, apps, memberships) can seem small individually, but dozens of $10–$20 charges can consume hundreds per year.

Quick action: once a quarter, list every subscription you have and decide if each one is still worth it.

🔹 4. Fees Are Hidden Expenses

ATM fees and service charges are “silent expenses” that drain cash without improving your financial life. Most people don’t notice them.

Quick action: if ATM fees appear often, consider switching to a bank with free ATM access or reimbursements.

🔹 5. Interest Shows Savings Progress

Even a dollar of interest means your savings are working—slowly. Use this as motivation to increase your high-yield savings rate or balance.

🚨 Spotting Red Flags in This Example

- multiple ATM fees

- timing risk between income and bills

- recurring expenses stacking up

- low automated savings

- minimal interest growth

Each of these is a potential improvement opportunity—not a problem.

💡 What This Example Tells Us About Financial Health

If this were your statement, you’d immediately know:

- when your income hits

- how much goes to basics vs lifestyle

- how many recurring subscriptions you carry

- whether you’re leaking money through ATM/maintenance fees

- how effectively your savings are growing

This kind of month-to-month review helps you build awareness and turn information into confident financial decisions.

✋ Quick Self-Check

Ask yourself:

- Is my income predictable each month?

- Do I know my average grocery spend?

- How many subscriptions do I have?

- Am I paying avoidable bank fees?

- Is money consistently going into savings?

If any answer is “no,” that’s a simple place to start.

🎯 Turning Insight Into Action (in 2 minutes)

Try this:

- Highlight all recurring charges

- Total them up

- Cancel any you don’t use

- Move that amount into savings each month

This single 2-minute habit can free up $300–$1,000 per year without changing anything else in your budget.

📌 Why This Example Matters

You’re not just reading numbers—you’re learning to interpret patterns, behaviors, timing, and progress. When you learn to “read between the lines,” your bank statement becomes a personal financial dashboard instead of a confusing document.

15. Common Questions Answered

Navigating through the maze of numbers and terms in a bank statement can often lead to questions. This interactive section aims to answer some of the most common queries you might have about your bank statements, enhancing your understanding and ability to manage your financial records effectively.

- What is the difference between ‘current balance’ and ‘available balance’?

- Current Balance refers to the total amount in your account at any given time, including pending transactions.

- Available Balance is the amount available for withdrawal or use, accounting for holds and pending transactions.

- Why do some transactions appear as pending on my statement?

- Transactions are often marked as pending because they have been authorized but not yet fully processed by the merchant. This is common with card transactions.

- How can I identify fraudulent transactions on my statement?

- Look for unfamiliar transactions, especially small ones (fraudsters sometimes test with small amounts). Report anything suspicious to your bank immediately.

- Can I dispute a transaction on my bank statement?

- Yes, if you identify a transaction that you believe is an error or fraudulent, contact your bank as soon as possible to dispute it.

- How can I use my bank statement to improve my credit score?

- Regularly review your statement to ensure timely payments and manage your credit utilization effectively, which are key factors in credit scoring.

- Why do I have overdraft fees, and how can I avoid them?

- Overdraft fees occur when you spend more than your account balance. Avoid them by keeping track of your spending and setting up account alerts.

- What should I do if I find an error on my bank statement?

- Contact your bank immediately to report the error. Provide as much detail as possible, including transaction dates and amounts.

- Understanding your bank statement is crucial for financial literacy and managing your money effectively. By addressing these common questions, we hope to provide you with the knowledge and confidence to navigate your financial journey. If you have more questions, feel free to reach out or comment below. Your insights not only help us improve our content but also aid other readers in their financial journey.

What budgeting strategies have worked for you after analyzing your spending patterns?

Budgeting Calculator

Conclusion

As we conclude our journey through decoding your bank statements, it’s important to reflect on the key insights gained. Understanding your bank statement is not just about keeping tabs on your account activity; it’s a critical step in mastering your personal finances. By demystifying the numbers and terms, you can take control of your financial health, identify areas for improvement, and make informed decisions that align with your financial goals.

Call to Action

- Stay Informed: Subscribe to [Your Blog Name] for more insights and tips on personal finance.

- Join the Conversation: Share your experiences and questions in the comments section below or our forums. Your input helps build a community of financial literacy.

- Spread the Word: If you found this post helpful, share it with friends and family who might benefit from it.

Remember, the path to financial wellness begins with understanding and actively managing your finances. Your bank statement is a window into your financial world; use it wisely to pave the way towards a secure financial future.

Thank you for joining us on this financial journey. We look forward to continuing to provide you with valuable content that helps you navigate the world of personal finance.

🔗 Continue Your Financial Learning Journey

Understanding your bank statement is just the beginning. To build stronger financial awareness, explore these related guides:

📊 Deepen Your Understanding of Financial Statements

- Decoding Business Financial Statements – Learn how businesses track income, expenses, and profitability

- Personal Financial Statements Guide – Understand your net worth, cash flow, and financial position

- Financial Planning Roadmap – A clear framework to help you build financial stability in logical stages.

- Life Insurance Planning Hub – Explore foundational insurance principles and strategic planning considerations.

📘 Build Your Financial Literacy Foundation

- → Return to Reading and Analyzing Financial Statements

- → Explore the Financial Education & Literacy Hub for step-by-step learning paths