⚖️ Term vs. Permanent Life Insurance: Key Differences, Costs, and How to Choose

Introduction

Choosing between term and permanent life insurance is one of the most important decisions in financial planning. Each type of policy serves a different purpose, and understanding the differences can help you select coverage that aligns with your financial goals, timeline, and budget.

⚡ Quick Answer: Term vs. Permanent Life Insurance

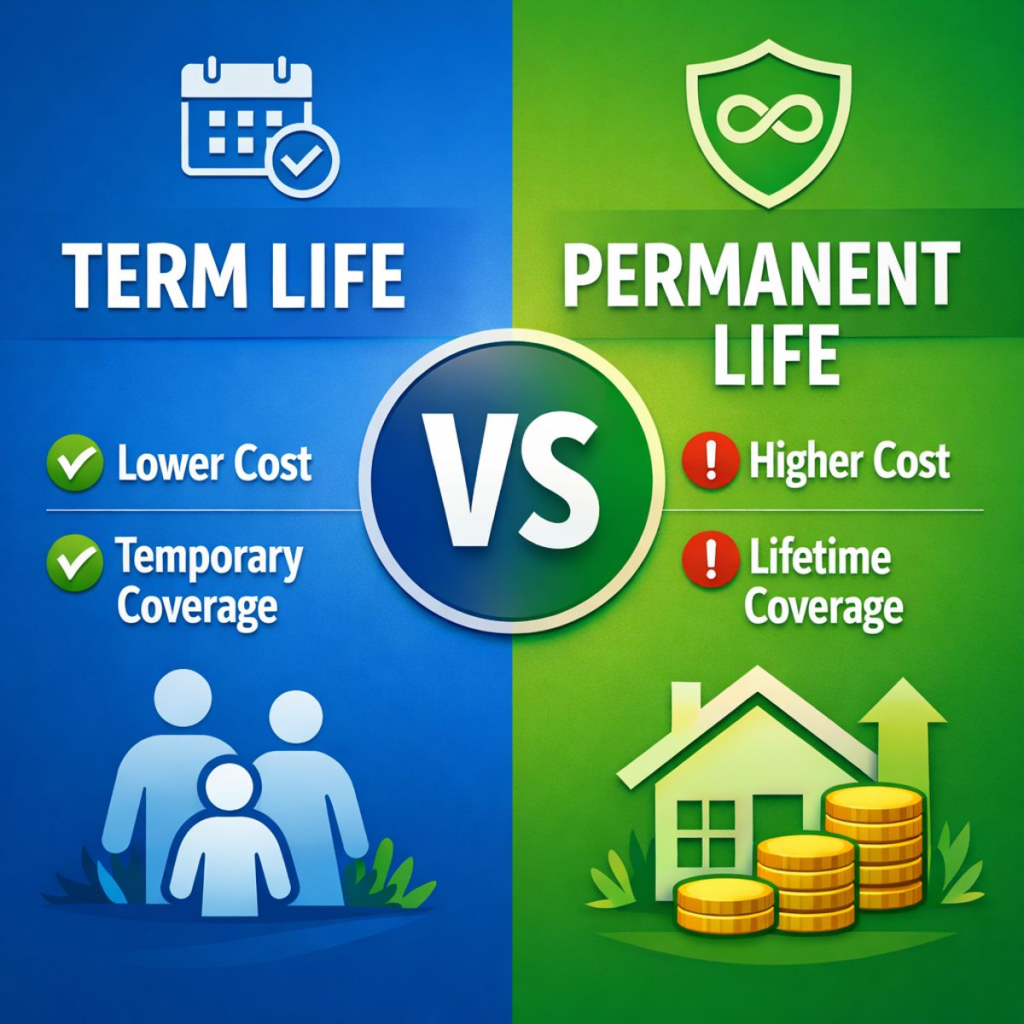

Term life insurance provides temporary, affordable coverage for a specific period—typically 10 to 30 years—making it a practical choice for income protection and time-bound financial obligations.

Permanent life insurance, on the other hand, offers lifetime coverage with higher costs and a more complex structure, making it better suited for long-term financial planning needs.

🔑 Key Takeaways

- Term life insurance = lower cost and temporary protection

- Permanent life insurance = lifetime coverage with higher cost

- The best choice depends on your financial goals and timeline

- Most households benefit from term life insurance for income protection

- Permanent policies may be appropriate for long-term planning needs

📊 Term vs. Permanent Life Insurance Comparison

| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Coverage Duration | Fixed term (10–30 years) | Lifetime coverage |

| Cost | Lower premiums | Higher premiums |

| Cash Value | None | Builds cash value over time |

| Complexity | Simple and straightforward | More complex structure |

| Best For | Income protection, temporary needs | Long-term planning, legacy goals |

| Flexibility | Limited | More flexible (loans, riders, adjustments) |

| Investment Component | No | Yes (varies by policy type) |

🟦 What Is Term Life Insurance?

Term life insurance is designed to provide financial protection during a specific period of time, making it one of the most straightforward and widely used types of life insurance.

🧠 How It Works

- Coverage lasts for a fixed term, typically 10, 20, or 30 years

- If the insured passes away during the term, the policy pays a death benefit to beneficiaries

- If the term expires without a claim, coverage ends unless renewed or replaced

📊 Key Benefits

- Affordable premiums compared to permanent life insurance

- Simple structure, making it easy to understand

- Flexible term lengths to match financial obligations

👉 Learn more: Term Life Insurance

🟩 What Is Permanent Life Insurance?

Permanent life insurance is designed to provide lifetime financial protection, as long as premiums are maintained. Unlike term life insurance, which expires after a set period, permanent policies remain in force indefinitely.

🧠 How It Works

- Coverage lasts for your entire lifetime, not just a fixed term

- The policy pays a death benefit to beneficiaries whenever the insured passes away

- Permanent life insurance includes several types, most commonly:

- Whole life insurance

- Universal life insurance

👉 Learn more:

📊 Key Characteristics

- Long-term protection designed to last a lifetime

- Higher cost compared to term life insurance

- More complex structure, often requiring deeper understanding and planning

Permanent life insurance is typically used when coverage is needed beyond temporary financial obligations.

💰 Cost Comparison: Term vs. Permanent Life Insurance

Cost is one of the most significant differences between term and permanent life insurance, and understanding why helps you make a more informed decision.

🟦 Why Term Life Costs Less

- Provides temporary coverage for a defined period

- Lower long-term risk for the insurer

- Simpler structure without lifetime guarantees

🟩 Why Permanent Life Costs More

- Provides lifetime coverage

- Includes long-term guarantees and structured protection

- Designed for extended financial planning

💰 Cost Comparison: Term vs. Permanent Life Insurance

| Factor | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Premium Level | Lower | Higher |

| Coverage Length | Temporary | Lifetime |

| Cash Value Funding | None | Included in premium |

| Administrative Costs | Lower | Higher |

| Investment Features | Not included | Included |

| Long-Term Cost | Lower overall | Higher but with additional benefits |

👉 Learn more: Life Insurance Cost Guide

💡 Key Insight

While permanent life insurance offers lifetime coverage, the higher cost may not be necessary for all individuals, especially those focused on temporary financial protection.

🧠 When Term Life Insurance Makes More Sense

Term life insurance is often the most practical option when your financial needs are time-bound and cost-sensitive.

📌 Term Life Is Often a Better Fit When You Need:

- Income protection for your family during working years

- Mortgage coverage or other large debts

- Financial support while raising children

- Budget-conscious planning with affordable premiums

For many households, term life insurance provides the most efficient way to manage financial risk without overextending your budget.

⚖️ Should You Choose Term or Permanent Life Insurance?

Choosing between term and permanent life insurance isn’t about which product is “better”—it’s about which solution fits your financial situation, goals, and timeline.

For most households, the decision comes down to a simple question:

👉 Are you trying to protect income for a specific period, or are you solving a long-term financial planning need?

Understanding that distinction can help you avoid overpaying for coverage—or underinsuring what matters most.

🧠 The Core Decision Framework

At a high level:

- Term life insurance is designed for temporary protection

- Permanent life insurance is designed for lifetime coverage and long-term planning

Here’s how that translates into real-world decision-making:

🟦 Choose Term Life Insurance If Your Priority Is Protection

Term life is often the best choice when your goal is to replace income and protect your family during your working years.

It typically makes the most sense if:

- You need affordable coverage with a high death benefit

- Your financial obligations are time-bound (mortgage, raising children, income replacement)

- You are still building wealth and prioritizing flexibility

- You want to maximize coverage per dollar

👉 For most families, term life provides the highest level of protection at the lowest cost, which is why it’s often the foundation of a financial plan.

🟩 Choose Permanent Life Insurance If Your Needs Extend Beyond Protection

Permanent life insurance may be appropriate when your goals go beyond income replacement and into long-term financial planning.

It may make sense if:

- You have a need for lifetime coverage

- You are focused on estate planning or legacy goals

- You want to accumulate cash value within a policy

- You have already built a strong financial foundation (emergency fund, retirement savings, etc.)

- You can comfortably afford the higher premiums over time

👉 Permanent policies are less about pure protection and more about strategic financial positioning over decades.

⚖️ The Reality for Most Households

For the majority of people:

- Term life insurance is the starting point—and often the primary solution

Permanent insurance, if used, typically plays a secondary or supplemental role rather than replacing term coverage entirely.

In many cases, the decision is not either/or—it’s when and how to layer coverage appropriately as your financial life evolves.

📊 A Practical Way to Think About It

- If losing your income would create financial hardship → Start with term

- If you’re solving long-term planning, tax, or legacy concerns → Consider permanent

- If you’re unsure → Start simple and build over time

🧠 Simple Decision Framework

| If Your Situation Is… | Recommended Option |

|---|---|

| You need affordable coverage for income protection | Term Life Insurance |

| You have young children or a mortgage | Term Life Insurance |

| You want lifetime coverage | Permanent Life Insurance |

| You are focused on estate or legacy planning | Permanent Life Insurance |

| You want flexibility and lower upfront cost | Term Life Insurance |

| You have strong financial foundation and want advanced planning | Permanent Life Insurance |

| You want balanced protection and long-term coverage | Combination of Both |

💡 Key Takeaway

The best life insurance decision is not about complexity—it’s about alignment.

- Term life insurance protects your present financial risks

- Permanent life insurance supports long-term financial strategies

Choosing the right one means understanding what problem you’re trying to solve today—and how that may change over time.

🧠 When Permanent Life Insurance May Make Sense

Permanent life insurance is not necessary for everyone, but it can be appropriate in certain situations—especially when your financial goals extend beyond temporary protection.

📌 Permanent Life Insurance May Be a Good Fit When You Need:

- Lifetime coverage needs

You want protection that does not expire and remains in place regardless of age or future health changes - Long-term planning strategies

Your financial plan includes extended timelines that go beyond working years - Predictability preference

You value consistent structure and long-term stability in your financial planning

Permanent life insurance can be useful when your priority is long-term continuity and certainty, rather than short-term cost efficiency.

🧠 When It Makes Sense to Own Both

While term and permanent life insurance are often presented as an either-or decision, in practice, many well-structured financial plans use both types of coverage together.

This approach—sometimes called layering or blending coverage—allows you to match different financial risks with the appropriate type of protection.

⚖️ Why Combining Term and Permanent Coverage Can Work

Each type of policy solves a different problem:

- Term life insurance protects against temporary financial risks

- Permanent life insurance supports long-term planning and legacy goals

By combining them, you can:

- Maximize affordable protection today

- Maintain lifetime coverage for future needs

- Adapt your insurance strategy as your financial situation evolves

👉 Instead of choosing one or the other, you’re building a more flexible and targeted protection strategy

🧩 Common Strategy: Layering Coverage

A typical approach might look like this:

- A larger term life policy to cover:

- Income replacement

- Mortgage or major debts

- Child-rearing years

- A smaller permanent policy to cover:

- Final expenses

- Legacy or estate planning goals

- Long-term financial positioning

👉 This structure allows you to protect what matters now without overpaying for lifetime coverage you may not need at full scale

📊 Example Scenario

Consider a 35-year-old parent with young children:

- They purchase a 20- or 30-year term policy to protect their family during peak earning years

- At the same time, they maintain a smaller permanent policy designed to remain in place for life

Over time:

- The term policy covers the highest-risk years

- The permanent policy remains as a long-term asset and legacy tool

🔄 Another Approach: Start Term, Add Permanent Later

Not everyone needs both policies immediately.

A common progression is:

- Start with term life insurance for affordability and protection

- Build savings, investments, and financial stability

- Add permanent coverage later as long-term planning needs become clearer

👉 This approach keeps your plan simple early on while preserving flexibility for the future

⚠️ When This Strategy May NOT Make Sense

Owning both types of insurance only works if it fits your financial reality.

It may not be appropriate if:

- You’re stretching your budget to afford premiums

- You haven’t yet built an emergency fund

- You’re behind on retirement savings

- The permanent policy is being used as a substitute for basic financial planning

👉 Insurance should support your financial plan—not compete with it

💡 Key Takeaway

Using both term and permanent life insurance can be a powerful strategy—but only when each piece has a clear purpose.

- Term insurance protects your highest-risk years

- Permanent insurance supports your long-term financial goals

The key is not complexity—it’s intentional design aligned with your financial plan

📊 Scenarios: Choosing the Right Policy

Understanding the differences between term and permanent life insurance is important—but applying those concepts to real-life situations is where clarity truly comes from.

The right choice depends on your life stage, financial responsibilities, and long-term goals. Below are practical scenarios that illustrate how different types of coverage can fit into a financial plan.

👨👩👧 Scenario 1: Young Family With Dependents

Situation:

- Age 30–40

- Married with young children

- Mortgage and primary income earner

Primary Goal:

Protect the family from income loss during working years

Best Fit:

👉 Term life insurance

Why it works:

- Provides high coverage at a low cost

- Aligns with time-bound needs (raising children, paying off a home)

- Maximizes financial protection during the most vulnerable years

💡 In this stage, affordability and coverage amount matter more than lifetime features.

🏠 Scenario 2: Mid-Career Professional With Growing Assets

Situation:

- Age 40–55

- Increasing income and savings

- Retirement planning underway

Primary Goal:

Balance protection with long-term financial planning

Best Fit:

👉 Combination of term and permanent life insurance

Why it works:

- Term insurance continues to provide income protection

- Permanent coverage introduces lifetime protection and cash value potential

- Allows for a gradual transition into more advanced planning strategies

💡 This is often the stage where layering coverage begins to make sense.

💼 Scenario 3: High-Income Earner Focused on Long-Term Planning

Situation:

- High income with maxed retirement accounts

- Strong financial foundation already in place

Primary Goal:

Enhance long-term financial strategies and legacy planning

Best Fit:

👉 Permanent life insurance

Why it works:

- Provides lifetime coverage

- Can be used as part of a broader financial strategy

- Supports estate planning and wealth transfer goals

💡 At this level, insurance becomes more strategic than purely protective.

🧓 Scenario 4: Pre-Retirement or Retirement Planning

Situation:

- Age 55+

- Mortgage mostly paid off

- Focus shifting to retirement income and legacy

Primary Goal:

Cover final expenses and leave a financial legacy

Best Fit:

👉 Permanent life insurance (if needed)

Why it works:

- Ensures coverage remains in place regardless of age

- Helps address final expenses and legacy goals

- Eliminates the risk of coverage expiring

💡 Term insurance often becomes less relevant unless a specific short-term need remains.

👤 Scenario 5: Single Individual With No Dependents

Situation:

- No children or financial dependents

- Early or mid-career

Primary Goal:

Minimal coverage or future flexibility

Best Fit:

👉 Limited term coverage (or none, depending on needs)

Why it works:

- Keeps costs low while covering basic obligations (debts, co-signed loans)

- Provides flexibility as life circumstances change

💡 Life insurance needs often increase later with family or financial responsibilities.

⚠️ Scenario 6: Overbuying Permanent Insurance Too Early

Situation:

- Early career

- Limited savings

- Sold a large permanent policy

Primary Risk:

Overcommitting to high premiums

Better Approach:

👉 Start with term life insurance

Why:

- Frees up cash flow for:

- Emergency savings

- Debt reduction

- Retirement investing

- Avoids financial strain from unnecessary complexity

💡 The biggest mistake is buying the wrong type of policy at the wrong time.

💡 Key Takeaway

There is no one-size-fits-all answer—only the right fit for your situation.

- Term life insurance is typically best for income protection and early-stage planning

- Permanent life insurance becomes more relevant as financial complexity and long-term goals increase

- A combination approach often works best as your financial life evolves

The key is to align your coverage with your current needs while staying flexible for the future.

🔄 Conversion Options: Term to Permanent Life Insurance

Many term life insurance policies include a conversion option, allowing you to convert some or all of your coverage into a permanent policy—without undergoing a new medical exam.

This feature adds flexibility and can be a powerful planning tool.

🧠 How Conversion Works

- You start with a term life policy

- During a specified period, you can convert it into a permanent policy

- No new underwriting is required, regardless of changes in health

👉 This locks in your future insurability

📊 Why Conversion Can Be Valuable

1. Health Protection

If your health declines, conversion allows you to secure permanent coverage you might not otherwise qualify for.

2. Flexibility Over Time

You can start with affordable term coverage and transition later as your financial situation evolves.

3. Gradual Strategy Shift

Some policies allow partial conversions, letting you maintain term coverage while adding permanent protection.

⚠️ Important Considerations

- Conversion windows are often time-limited

- Premiums for permanent coverage will be higher at conversion

- Policy options available for conversion may be restricted

👉 Understanding your policy’s conversion terms early is critical

💡 Key Takeaway

Conversion options provide flexibility—but they are not automatic solutions.

They work best when used as part of a planned transition, not a last-minute decision.

🧩 Riders and Policy Customization Options

Life insurance policies are not one-size-fits-all. Most policies can be customized using riders—optional features that modify or enhance your coverage to better match your financial needs.

Riders allow you to tailor a policy beyond the base structure, adding flexibility and protection for specific risks.

🧠 What Are Riders?

A rider is an add-on provision that changes how your policy works. Some riders increase coverage, while others provide access to benefits under certain conditions.

They typically come at an additional cost, though some may be included depending on the policy.

📊 Common Life Insurance Riders

1. Accelerated Death Benefit Rider

- Allows access to a portion of the death benefit if diagnosed with a terminal illness

- Helps cover medical or end-of-life expenses

2. Waiver of Premium Rider

- Waives premiums if you become disabled and unable to work

- Keeps your policy active without financial strain

3. Child Term Rider

- Provides coverage for your children under the same policy

- Can often be converted to permanent coverage later

4. Guaranteed Insurability Rider

- Allows you to increase coverage at specific times without additional medical underwriting

- Valuable if your health may change in the future

5. Return of Premium Rider (Term Policies)

- Refunds some or all premiums if you outlive the term

- Higher upfront cost, but appeals to those wanting a “use-it-or-get-it-back” structure

⚖️ When Riders Make Sense

Riders can be valuable when they align with a specific need:

- Protecting against loss of income due to disability

- Planning for future insurability changes

- Adding flexibility without buying a new policy

👉 The key is intentional use—not adding features simply because they’re available.

💡 Key Takeaway

Riders can enhance a policy—but they also increase complexity and cost.

The goal is not to build the most feature-rich policy, but to design one that efficiently covers your most important risks.

⚠️ What Happens If a Policy Lapses?

A life insurance policy lapses when premiums are not paid and the policy is no longer in force.

When this happens, coverage ends, and your beneficiaries may no longer receive a death benefit.

🧠 What Causes a Policy to Lapse?

- Missed premium payments

- Insufficient cash value (for certain permanent policies)

- Policy loans reducing available value

📊 What Happens Next?

For Term Life Insurance:

- Coverage simply ends

- No payout or residual value

For Permanent Life Insurance:

- The policy may:

- Use remaining cash value to cover premiums temporarily

- Enter a grace period

- Eventually terminate if funding is insufficient

⚠️ Potential Consequences

- Loss of coverage when it’s needed most

- Difficulty obtaining new coverage due to age or health changes

- Loss of premiums already paid

👉 In some cases, reinstatement may be possible—but often requires proof of insurability.

💡 Key Takeaway

A lapse is not just a missed payment—it’s a loss of financial protection.

Maintaining your policy is essential to ensuring it performs its intended role in your financial plan.

⚠️ Pros and Cons of Each Option

Understanding the trade-offs between term and permanent life insurance helps you make a more informed and balanced decision.

🟦 Term Life Pros and Cons

✅ Pros

- Affordable

Typically offers the lowest cost for coverage - Simple

Easy to understand and manage

⚠️ Cons

- Temporary

Coverage ends after the term expires - Expires

May require renewal or replacement later in life

🟩 Permanent Life Pros and Cons

✅ Pros

- Lifetime coverage

Provides protection that does not expire - Stability

Designed for long-term consistency and predictability

⚠️ Cons

- Higher cost

Premiums are significantly higher than term life insurance - More complex

Requires a deeper understanding and ongoing attention

🧠 Key Takeaway

Term life insurance focuses on affordability and temporary protection, while permanent life insurance emphasizes long-term stability and lifetime coverage.

The best choice depends on your financial goals—not just the features of the policy.

⚖️ Pros and Cons Comparison

| Term Life Insurance | Permanent Life Insurance | |

|---|---|---|

| Pros | Lower cost Simple structure High coverage amounts Ideal for temporary needs | Lifetime coverage Builds cash value More flexible features Supports long-term planning |

| Cons | Coverage expires No cash value No return if unused | Higher cost More complex Requires long-term commitment Risk if mismanaged |

🧾 How to Choose Between Term and Permanent Life Insurance

Choosing the right life insurance policy depends on your financial situation, long-term goals, and budget. There is no one-size-fits-all answer—the best choice is the one that aligns with your needs today and remains sustainable over time.

🧭 Key Questions to Ask

Before deciding, consider these essential questions:

- How long do I need coverage?

Are you protecting temporary obligations, or do you need lifetime coverage? - What can I afford long-term?

Can you comfortably maintain premium payments over time? - What are my financial goals?

Are you focused on income protection, long-term planning, or both?

Taking the time to answer these questions can help you avoid unnecessary complexity and choose a policy that fits your overall financial plan.

📊 Simple Decision Framework

Use this straightforward approach to guide your decision:

- Temporary financial needs → Term Life Insurance

- Long-term or lifetime needs → Permanent Life Insurance

This framework helps simplify what can otherwise feel like a complex decision.

👉 Start here: How Much Life Insurance Do You Need?

🔄 Term + Permanent Strategy (Layering Approach)

| Strategy Component | Role in Financial Plan |

|---|---|

| Term Life Insurance | Covers income replacement and major financial risks during working years |

| Permanent Life Insurance | Provides lifetime coverage and supports long-term financial goals |

| Combined Strategy | Balances affordability today with long-term planning and legacy needs |

⚠️ Common Mistakes When Comparing Policies

Many individuals make avoidable mistakes when choosing between term and permanent life insurance. Being aware of these pitfalls can help you make a more confident and informed decision.

- Choosing based on price alone

Lower cost does not always mean better coverage for your needs - Overcomplicating your decision

More complex policies are not always necessary - Not aligning with long-term goals

Your policy should support your broader financial strategy - Ignoring affordability over time

A policy must remain sustainable—not just affordable today

💡 Key Takeaway

A well-chosen life insurance policy balances coverage, cost, and long-term financial alignment. Avoid rushing the decision, and focus on selecting a policy that fits your situation—not just the features on paper.

👉 Learn more: Common Life Insurance Mistakes

💡 Loans, Cash Value, and Policy Risks

Permanent life insurance policies that build cash value may allow you to borrow against that value.

While this can provide flexibility, it also introduces important risks.

🧠 How Policy Loans Work

- You borrow against the policy’s cash value

- The loan does not require a credit check

- Interest accrues on the borrowed amount

👉 The policy itself acts as collateral

📊 Potential Benefits

- Access to liquidity without selling investments

- Flexible repayment terms

- No immediate tax implications in many cases

⚠️ Key Risks to Understand

1. Reduced Death Benefit

Any outstanding loan balance (plus interest) reduces what beneficiaries receive.

2. Compounding Interest

Unpaid interest increases the loan balance over time.

3. Risk of Policy Lapse

If the loan grows too large relative to the cash value, the policy may lapse.

4. Potential Tax Consequences

If a policy lapses with an outstanding loan, it may trigger taxable income.

⚖️ When Loans May Be Appropriate

Policy loans can be useful when:

- Used strategically and monitored closely

- Integrated into a broader financial plan

- Not relied upon as a primary funding source

💡 Key Takeaway

Policy loans provide flexibility—but they are not “free money.”

They must be managed carefully to avoid undermining the very protection the policy was designed to provide.

❓ Frequently Asked Questions

Which is better, term or permanent life insurance?

There is no universal “better” option—it depends on your goals.

- Term life insurance is often the better choice for most households because it provides affordable, temporary protection during key financial years.

- Permanent life insurance may be appropriate if you need lifetime coverage or have long-term planning considerations.

The right choice is the one that aligns with your financial timeline, budget, and overall plan.

Why is permanent life insurance more expensive?

Permanent life insurance costs more because it provides:

- Lifetime coverage instead of temporary protection

- Long-term guarantees that extend beyond a fixed term

- A more structured and complex policy design

These features increase the long-term cost compared to term life insurance, which is designed for shorter durations.

Can you switch from term to permanent life insurance?

In some cases, yes. Certain term life policies include a conversion option, allowing you to transition to a permanent policy without undergoing a new medical evaluation.

However:

- Conversion terms vary by policy

- Costs typically increase when converting

- It’s important to review the details carefully

📚 Related Life Insurance Articles

Continue exploring related topics to deepen your understanding and support your decision-making.

📰 Featured Articles

- Term vs. Whole Life Insurance

Compare two of the most common policy types and understand when each may be appropriate - Life Insurance Cost Breakdown

Learn what factors influence premiums and how to estimate your costs - How Much Life Insurance Do You Need?

Discover how to calculate coverage based on income, debt, and financial goals

-

How to Cash Out Life Insurance (Without Costly Mistakes): Options, Taxes, and Smart Strategies

💡 Quick Answer: Can You Cash Out Life Insurance? Yes—but only certain types of policies allow you to access cash value. ✅ Permanent Life Insurance (Whole, Universal, Variable) Policies such as whole life, universal life, and variable life insurance build cash value over time, which you can access in several ways: ❌ Term Life Insurance […]

-

How Life Insurance Supports Estate Planning: A Complete Guide to Protecting Your Family and Legacy

1. Introduction – Why Life Insurance Is a Critical Estate Planning Tool Estate planning is ultimately about preparing your family for the future—financially, legally, and emotionally. It ensures that your assets are protected, your wishes are honored, and the people you care about are supported long after you’re gone. Yet even the strongest estate plan […]

-

Understanding Permanent Life Insurance: Types, Costs, Cash Value & Long-Term Benefits

1. Introduction: What Makes Insurance “Permanent”? Permanent life insurance refers to a category of policies designed to provide lifelong coverage while also building cash value over time. Unlike term insurance—which expires after a set period—permanent life insurance stays in force for your entire lifetime as long as required premiums are paid. That lifetime promise is […]

-

A Complete Guide to Term Life Insurance – How It Works, What It Covers, and When You Need It

1. What Is Term Life Insurance? Definition and purpose Term life insurance is a form of life insurance that provides a death benefit for a set number of years, known as the “term.” If death occurs during this period and the policy is active, beneficiaries receive a lump-sum payout. The primary purpose is income protection […]

🔗 Next Steps

Take the next step by exploring specific policy types and building a plan that fits your financial situation.

🧭 Start Here

- Term Life Insurance

Understand how affordable, temporary coverage can protect your income and financial responsibilities - Whole Life Insurance

Explore lifetime coverage options designed for long-term financial planning and stability

🚀 Continue Learning

- Life Insurance Cost

Dive deeper into pricing factors and how to estimate premiums - How to Buy Life Insurance

Follow a step-by-step process to compare policies and choose the right coverage - Life Insurance Is It Worth It?

🏁 Final Thought

Choosing between term and permanent life insurance doesn’t have to be complicated. By focusing on your financial goals, timeline, and budget, you can simplify the decision and select coverage that truly fits your needs.

The most effective strategy is to align your policy with your overall financial plan—protecting what matters most while avoiding unnecessary complexity or cost.